•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Quang Ngai Sugar Joint Stock Company (UPCoM: QNS) remains a leading player in Vietnam’s soy milk market and is also one of the country’s largest sugar producers. With Vietnam’s sugar industry still under pressure from price and demand conditions, the soy milk segment continues to play a stabilizing role in supporting the company’s overall business results.

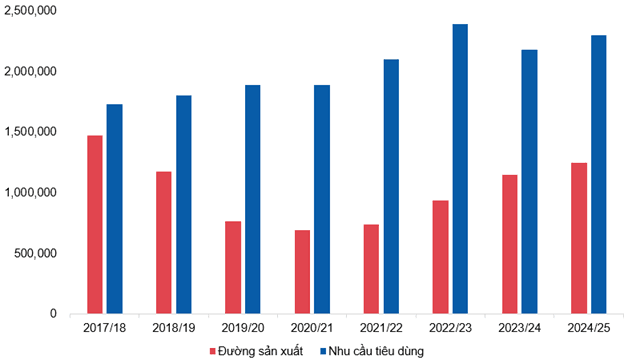

According to the Vietnam Sugarcane and Sugar Association (VSSA), the 2024/25 crop year saw a rebound in the sugar industry. The harvested sugarcane area exceeded 189,000 hectares, while cane crushing output reached 12.4 million tons, up more than 16% year-on-year. As a result, sugar production rose to over 1.26 million tons, up 14.3% year-on-year.

Domestic consumption remains high at an estimated 2.2–2.4 million tons per year. However, domestic supply currently meets only about 55% of demand, leaving a sizable supply-demand gap.

In 2026, global sugar prices continued to trend downward versus the previous year, fluctuating around 13.5–14.5 US cents per pound. The decline reflects increased supply pressure from major producers including Brazil, India, and Thailand, while demand has not yet shown a clear rebound.

Despite the downward trend, sugar prices are expected to reverse higher in the near term due to rising cane use for ethanol production, which could tighten sugar supply. Additional risks include potential supply chain disruptions tied to geopolitical factors, and a less favorable outlook for the next crop year as El Nino is expected to return later in 2026.

Against the backdrop of sustained low sugar prices, QNS’s sugar segment in 2025 delivered weaker performance. Revenue reached VND 3,629.9 billion, down 7.9% from 2024, and the segment’s contribution to total revenue fell to 35.2%.

Profitability also declined more sharply. Gross profit decreased to VND 770.8 billion, down 40.2% year-on-year, narrowing the gross margin to 22% from the previous year.

The article attributes the weaker results mainly to:

To respond to pressures in the sugar industry, QNS continued strengthening its production base by expanding its raw material area. The 2024/25 crop year saw sugarcane area reach 31,599 hectares, up 9% year-on-year, indicating a shift toward greater long-term self-sufficiency.

QNS’s raw material base is currently concentrated mainly in Gia Lai and Quảng Ngãi, at about 30,000–32,000 hectares. The company aims to expand to 40,000 hectares in the 2027–2028 crop year.

In addition, the An Khê sugar mill increased crushing capacity from 18,000 tons to about 25,000 tons per day since the 2025–2026 crop year.

While the sugar segment faced challenges, the soy milk division continued to act as QNS’s pillar. In 2025, the segment maintained stable growth and contributed a large share to revenue, becoming the main driver supporting the company’s revenue and helping stabilize overall business results.

QNS currently imports about 70–80% of its soybeans, making the company directly exposed to world price movements. After a cooling period in 2023–2025, soybean prices have risen again amid increasing geopolitical tensions, which could raise the risk of cost volatility in the near term.

Nevertheless, with a stable consumption base and market leadership, the soy milk segment remains the profit backbone of QNS and is expected to maintain growth in 2026.

[Enterprise Analysis Department, Vietstock Advisory]

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…