•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

As of May 4, 2026, 803 listed banks and companies—representing about 97% of total market capitalization—have published financial statements or preliminary estimates for Q1 2026 results, with after-tax profit growth year over year remaining solid at +38.2%, according to statistics from FiinTrade.

Growth was led by the non-financial group, rising 69.8% year over year, well ahead of the financial group (+14.4%). Within the financial sector, banks posted profit growth of +13.7%, the lowest in several quarters. The slower performance was attributed to pressure from a narrowing net interest margin (NIM) and slower credit growth.

By market capitalization, the mid-cap VNMID group remained the main driver of profit growth at +82.6% year over year, far ahead of the large-cap VN30 group (+27.4%). The small-cap VNSML group was nearly flat, with growth of +4.5%.

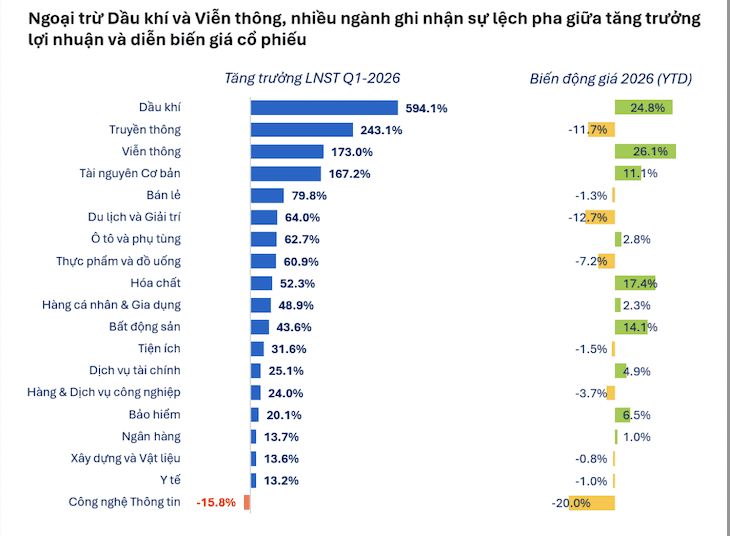

Sector performance was highly divergent. Profit growth was concentrated in cyclical sectors including Oil & Gas, Basic Resources, Retail, Food & Beverage, Chemicals, and Real Estate. By contrast, Information Technology declined, while sectors such as Banking, Securities, and Construction & Materials posted slower gains.

The profit mix continued to shift. The share of banks decreased from 46.3% to 38.1%, while Real Estate and goods-related sectors contributed more. This reflected a reduced leadership role for banks and a profit structure increasingly tilted toward cyclical sectors.

Stock price movements showed clear divergence across sectors, even though market-wide profit growth remained high in Q1/2026. With the exception of Oil & Gas and Telecommunications—where price movements and profit growth were relatively synchronized—most sectors recorded strong profit growth but less positive or flat price performance.

In particular, sectors such as Retail, Food & Beverage, Tourism, and Personal Goods reported profit growth of 50–80% year over year, yet their stock prices have fallen or moved sideways since the start of the year. This pattern suggests investors have been cautious about the sustainability of growth and prospects for consumer demand.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…