Analysts have issued positive recommendations for PHR, KDH, and NTC, citing growth drivers such as land compensation revenues from industrial parks, new project launches, and a stable dividend policy. The outlooks are anchored by forecasts for earnings growth and strategic developments in industrial park projects and real estate activities.

- PHR: Growth is driven by land compensation revenues from the industrial park and favorable rubber price trends.

- KDH: Positive outlook due to anticipated new project launches and earnings growth.

- NTC: Supportive outlook from Nam Tan Uyen 3 Industrial Park and a stable dividend policy.

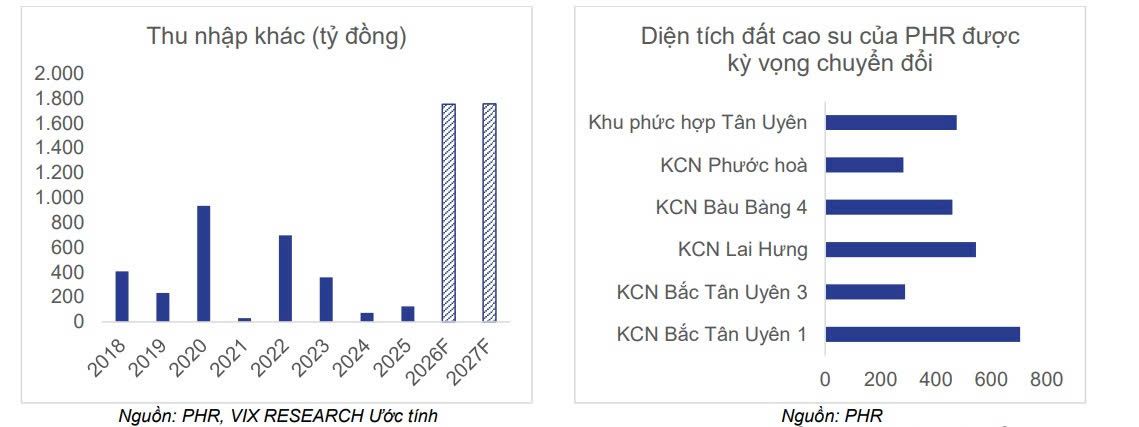

Analysts issued a buy rating with a target price of 75,900 dong per share. Vietstock Securities Joint Stock Company (VIX) forecasts PHR’s 2026 net profit at about 1,967 billion dong, up 296% from 2025. The growth is expected to be driven by land compensation from the industrial park and favorable rubber prices. Rubber futures in Japan have risen to around 434 JPY/ton, the highest in 10 years, supporting a 2026 rubber segment revenue forecast of about 1,954 billion dong, up 19% year-on-year. Additional income from converting rubber land to industrial parks is a major growth driver, with an estimated 3,511 billion dong in compensation from the North Tan Uyen 1 Industrial Park project and the remaining area at VSIP III in 2026–2027, equivalent to about 40% of the company’s current market capitalization. PHR also maintains a strong balance sheet with more than 2,063 billion dong in cash and short-term deposits and debt of around 22 billion dong. The company plans to pay stock dividends of 80% and cash dividends of 14%. The target price of 75,900 dong per share implies upside of about 22% from the market price around 62,000 dong on 25 June.

Dragon Capital Securities (VDSC) gives KDH a buy rating with a target of 41,500 dong per share. Q1 2026 net profit attributable to the parent was 281.4 billion dong, up 131% year-on-year, aided by a 285.2 billion dong gain on a bargain purchase after the transfer and consolidation of An Lập Real Estate Development Co. Ltd. The company also advanced land clearance for key projects, lifting finished goods value to 29,126 billion dong. To support M&A activity, legal improvements, and project execution, total outstanding debt rose to 15,348 billion dong. For Q2 2026, VDSC expects net revenue of about 374 billion dong, up 33% quarter-on-quarter, with a gross margin around 65%. Growth in the second half of 2026 is expected from the Gladia by the Waters high-rise subdivision launching in Q3 2026, with a selling price around 91 million dong per m². For the full year 2026, VDSC projects net revenue of 4,796 billion dong and net profit attributable to the parent of about 1,460 billion dong. Using RNAV-based valuation, VDSC sets a target of 41,500 dong per share.

ACBS provides a positive outlook for Nam Tan Uyên Industrial Park (NTC), with growth supported by the NTC3 project. Due to revenue recognition changes under Circular 99, 2026 plans are conservative, with revenue of 546 billion dong and pre-tax profit of 273 billion dong. Six-month results show revenue around 266 billion and pre-tax profit around 168 billion, achieving 49% and 62% of the annual targets respectively. ACBS notes NTC3 has total infrastructure investment of about 871 billion dong, which will be a long-term growth driver. Land handovers at year-start were about 6 hectares to ensure infrastructure readiness before leasing, and the company has signed memoranda with customers for more than 20 hectares. From July–August 2026, after infrastructure completion and environmental acceptance, NTC is expected to sign formal lease contracts at about 185 USD per m² for the remaining lease term. Accounting policy changes lead ACBS to revise 2026 net revenue to 515 billion dong and net profit to about 335 billion dong, up 4% year-on-year. The company is also expected to maintain cash dividends of 6,000 dong per share, implying a yield of about 4.4%. ACBS sets a target of 147,400 dong per share, implying a total expected return of about 12.8% versus the price of roughly 136,000 dong per share on 29 June.

The recommended targets indicate potential upside for PHR and NTC based on current price levels cited in the report, with PHR positioned by substantial land compensation income and rubber price trends, and NTC supported by the NTC3 project and solid dividend policy. KDH’s upside is framed within expectations of new project launches, improved profitability, and repayment/management of debt as part of expansion plans.

Analysts cited include Vietstock Securities Joint Stock Company (VIX) for PHR’s positive rating and target, Dragon Capital Securities (VDSC) for KDH’s buy recommendation and projected 2026 figures, and ACBS for NTC’s positive view, conservative 2026 plans, and dividend policy. The reports highlight earnings growth tied to real assets and industrial park developments, as well as disciplined capital management and dividend payments as key supports for investor interest.