•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

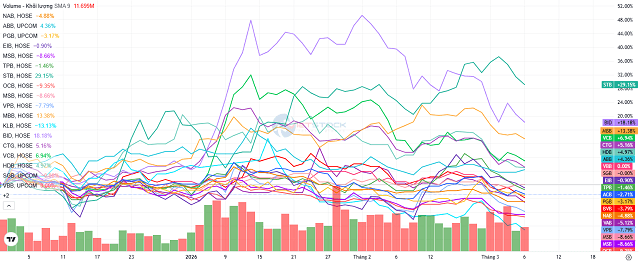

Bank stocks in April 2026 saw a notable rebound as the sector's total market capitalization rose by nearly 83,000 billion VND. Driven by the FTSE Russell market upgrade and a stable macro backdrop, gains spread across the board. Liquidity remained cautious with foreign selling continuing but easing to the lowest in three months, raising positive expectations for the next phase. Macro factors supporting and upgrade boost - The Vietnamese stock market recovered in April 2026. By April 29, VN-Index stood at 1,854.1 points, up 179.61 points (nearly 11%). The sector index for banks rose to 982.84 points, up 2.7%. - The biggest driver was FTSE Russell's upgrade of the market from Frontier Market to Secondary Emerging Market, expected to take effect in September 2026. This milestone is anticipated to trigger billions of dollars of foreign capital and raise Vietnam's standing on the global investment map. - In addition, macro factors in April continued to support the 'king' stocks. Q1 2026 GDP growth reached 7.83%, creating a solid psychological backdrop for investors. The State Bank kept lending rates at a moderate level to support business recovery and accelerate credit to the economy in Q2. The USD/VND exchange-rate pressure eased in April, combined with active FDI disbursement, reducing macro risk. - Coupled with positive Q1 2026 earnings results from many banks, overall banking sector market capitalization rose by 82,636 billion dong compared with the end of March, a 3.2% increase. - Bank index and VN-Index since early 2025 to early May 2026 (diagram) … Capitalization diverged - Nearly 63% of bank stocks rose in April (about 17 names higher than March). VBB led with a 26.42% capitalization rise, followed by LPB (+12.89%), KLB (+12.26%), and TCB (+10.26%). - In the state-owned bloc, BID led with a 5.53% increase, followed by VCB (+2.93%) and CTG (+1.01%). Liquidity: Diligent but cautious trading - Although stock prices rose, turnover remained modest. Average daily matched-trade volume exceeded 216 million shares, down 13% from March; matched-trade value fell to 5.225 trillion dong per day (down 17%). - Total trading value (including matched and negotiated) reached about 268 million shares per session, equivalent to 6.314 trillion dong per day (down 18%). - This reflected investor hesitation ahead of the VN-Index's psychological barrier, with funds choosing to wait rather than chase. Liquidity bright spots persisted: VBB and PGB saw liquidity surge. VBB's matched-trade volume and value jumped 5.3x and 6.9x respectively; PGB rose 2.2x in both metrics. SHB led sector liquidity with over 86 million shares traded daily (+14.84%), followed by HDB with over 20 million shares. - On the downside, BAB fell into a liquidity trough with average daily volume below 10,000 shares (down 42%). Foreign selling pressure cooled noticeably - April marked the third consecutive month of foreigners net selling banking stocks. However, aided by macro factors and upgrade news, selling slowed significantly. Total net selling in April was 5.566 trillion dong (about 190 million shares). - Selling pressure concentrated on large-cap stocks to restructure portfolios, with VCB the largest net seller (-1.293 trillion), followed by BID (-932 billion) and HDB (-698). - Foreign demand was thin, scattered across a few names such as LPB (238 billion), TPB (61), TCB (26), ABB (21) and OCB (14). Overall, with easing net selling and a bright macro outlook, banking stocks are building firmer foundations for further upside in the coming months of 2026. *(Mã chứng khoán liên quan and other sections follow in the original page beyond the main narrative.)

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…