On 06/07/2026, the market fluctuated around the 1,860-point level as investors weighed mixed signals from large-cap names and corporate actions. By midday, the VN-Index stood near 1,860.16 points, while the HNX-Index retreated to 300.29 points, down 2.37%. Market breadth favored the decliners with 385 stocks down and 204 up.

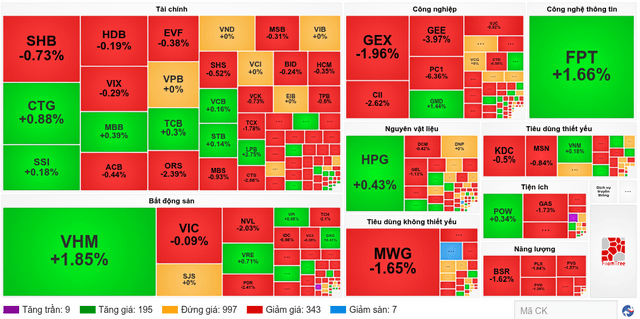

The session opened with the VN-Index moving higher to 1,873.03 points, up 10.95 points or 0.59%, led by gains in real estate and financials. Real estate, led by VHM following the rights issue news, helped push the index higher, while the broader market saw mixed moves as PNJ faced local pressure and bank shares rotated.

At 10:30, the market was in a tug-of-war, with real estate continuing to lead as foreigners sold heavily. The VN-Index posted only a modest net gain as selling pressure from foreign investors and declines in PNJ, GAS and consumer staples constrained a broader rally. The VN-Index showed cautious but not pessimistic sentiment, with blue chips like VHM, CTG, and FPT providing support.

Morning liquidity centered on real estate, with VHM contributing the most to turnover and price moves. VHM traded with matched value over 567 billion dong, rising 1.85% and adding 2.48 points to the VN-Index. VIC rose 0.09% (+0.32 points) on turnover over 129 billion dong amid ecosystem spillover from VinFast's new electric car under 190 million dong. The banking sector showed mixed performance, with CTG up 1.17% and VCB up 0.32%, while other banks faced selling pressure. The technology group saw FPT rise 1.38%, contributing 0.36 points with liquidity over 294 billion dong.

On the downside, GAS fell 1.99% and PNJ dropped 6.98%, the latter removing 0.41 points as a drag on the index. Consumer discretionary and industrials faced pressure from MCH (-1.28%) and MWG (-1.65%), and VJC declined 1.13%.

Foreign selling remained a challenge in the morning, with net selling exceeding 15.3 million shares, about 370 billion dong. VHM was the most traded stock with more than 45.3 billion dong bought and over 151 billion dong sold, indicating ongoing portfolio rotation after the rights issue. In addition, foreigners heavily sold SSI, VIB, HPG and MSB, while buying FPT, CTG, and VRE, signaling a preference for technology and quality banks.

Foreign selling and sector rotations weighed on the attempt to extend a recovery, with liquidity subdued across HOSE and Hanoi/UPCOM markets and money focused on blue-chip names. The news on VinHomes' rights issue and its effect on VHM contributed to both dilution expectations and investor confidence. The margin-cut decision by HOSE for 59 stocks added potential near-term selling pressure for selected names, including HVN, DGC and BCG.

Market breadth showed clear polarization, with gains and declines clustered around a few large-cap names. The morning pattern suggested money was flowing selectively rather than broadly, with real estate and technology leading the move while real estate, banks, and consumer staples faced selling pressure. Analysts note that the current environment indicates selective money flow rather than a broad market rally, and ongoing foreign selling will be a key factor to monitor for near-term direction.