•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Prosperity and Development Joint Stock Commercial Bank (PGBank) held its 2026 annual general meeting in Hanoi on April 21, outlining ambitious business targets for the year and seeking shareholder approval for a capital increase and plans to expand into securities.

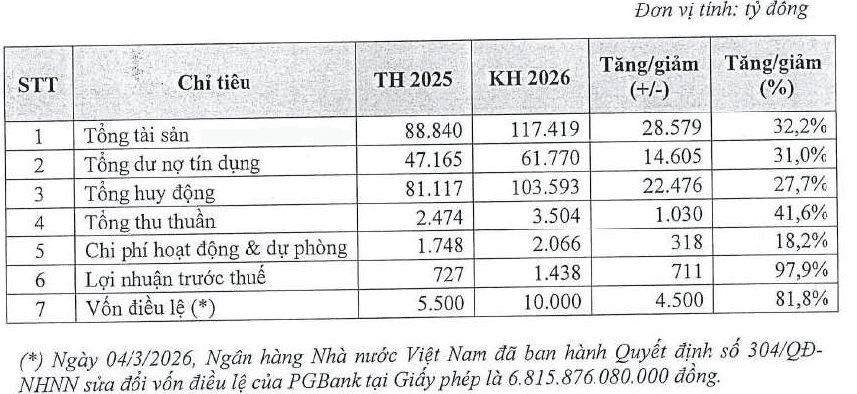

PGBank set a 2026 pre-tax profit target of 1,438 billion dong, up 97.9% from 2025. The bank also aims to expand total assets to 117,419 billion dong, up 32.2% year on year.

For credit and funding, PGBank expects lending to reach 61,770 billion dong (up 31%) and deposits to rise to 103,593 billion dong (up 27.7%).

On efficiency and risk metrics, the bank targets ROE of at least 12%, a CAR above 11%, and an NPL ratio below 2%, aiming to balance growth with safety in a dynamic business environment.

PGBank said it will focus lending on production and business activities, retail customers, and small and medium enterprises—segments it described as having remaining growth potential.

The bank also plans to accelerate digital transformation, upgrade technology infrastructure, and develop products and services to improve operational efficiency and customer experience in 2026.

In 2025, PGBank recorded pre-tax profit of 727 billion dong, which did not meet its plan. The bank attributed the shortfall primarily to weaker-than-expected net interest income and delays in recovering some debts sold to the Vietnam Asset Management Company (VAMC).

At the meeting, PGBank sought shareholder approval to raise its charter capital to 10,000 billion dong, nearly 1.5 times the current level, through share issuances to existing shareholders and a dividend in kind via shares.

The bank proposed issuing more than 318.4 million new shares, corresponding to about 3,184 billion dong in additional capital. After completion, charter capital would be 10,000 billion dong.

PGBank said all new shares would be freely transferable.

The bank stated the raised capital would support lending activities, investment, and strengthen its financial capacity, helping improve capital adequacy ratios under increasingly stringent requirements.

The meeting again approved the board’s intention to contribute capital, acquire shares, or establish or acquire a securities company to become a subsidiary of PGBank. The proposed securities business would be licensed to operate in securities underwriting, brokerage, investment advisory, and proprietary trading.

Previously, at the 2025 extraordinary general meeting, PGBank had approved similar capital contribution and acquisition options for establishing or acquiring a securities company, as well as an insurance firm, to expand into new fields as a subsidiary or affiliate.

Shareholders asked why 2025 results did not meet the plan. CEO Nguyen Van Huong said that while the year did not achieve the target, growth remained strong.

As of December 31, 2025, PGBank reported total assets of 88,840 billion dong, nearly 90 trillion; lending of around 47,000 billion dong; net interest income of about 2,400 billion dong; and profit of 727 billion dong, up 70.8% from 2024.

The CEO said the gap versus the 2025 profit target of 1,001 billion dong was due to market risks and monetary fluctuations, and the bank emphasized diversification of risk and continued focus on asset quality.

Shareholders asked about the 2026 credit growth target of about 31% and how it would be implemented. The CEO said it would depend on credit quotas approved by the State Bank of Vietnam, with priorities including export–import enterprises with foreign currency, SMEs supporting production and goods, and individuals/private households.

Shareholders also asked about Q1 2026 performance. By end-March 2026, PGBank reported total assets of 86,700 billion dong and deposits of 47,000 billion dong. Q1 profit was 275 billion dong, up 2.8 times from Q1 2025 (96 billion dong), representing about 19.2% of the annual plan.

The bank said the improvement was driven by non-interest income, especially services such as letters of credit, guarantees, insurance, and foreign exchange, along with recovery of some non-performing loans. It added that liquidity, asset quality, and credit management remained stable in Q1.

PGBank acknowledged that the 2026 profit target of 1,438 billion dong—a 97.9% increase from 2025—is challenging. To pursue it, the bank plans to implement coordinated growth initiatives linked to risk management and digital transformation.

These include personalized product development for key segments (such as trade finance for export/import, letters of credit, and payments collection), leveraging Big Data and AI to enhance cross-selling, and improving customer experience on a digital platform through a new core banking system and a connected digital banking app.

The bank also plans to expand its ecosystem through partnerships with fintech firms and digital platforms.

PGBank said it will pursue selective lending growth, prioritizing manufacturing and export/import, and tighten asset quality control using credit scoring and approval models. It also plans to accelerate debt resolution using technology and build early-warning systems.

In addition, the bank intends to invest in human resources by standardizing competency frameworks and developing incentive and training programs, while modernizing risk management driven by data. It will invest in technology, data, AI, automation, and information security, and improve financial management, marketing, and branding to support sustainable growth.

On technology strategy, PGBank said digital transformation is essential. In 2025, it invested heavily, including migrating the core banking system to a new platform, launching digital banking apps for retail and corporate clients, building open API connections, and investing in systems for capital markets and interbank operations. In 2026, it plans to continue developing digital products, standardize systems, enhance security, and ensure safe and efficient operations.

The meeting concluded with all proposals approved by a large majority. Source: Market Life.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…