•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

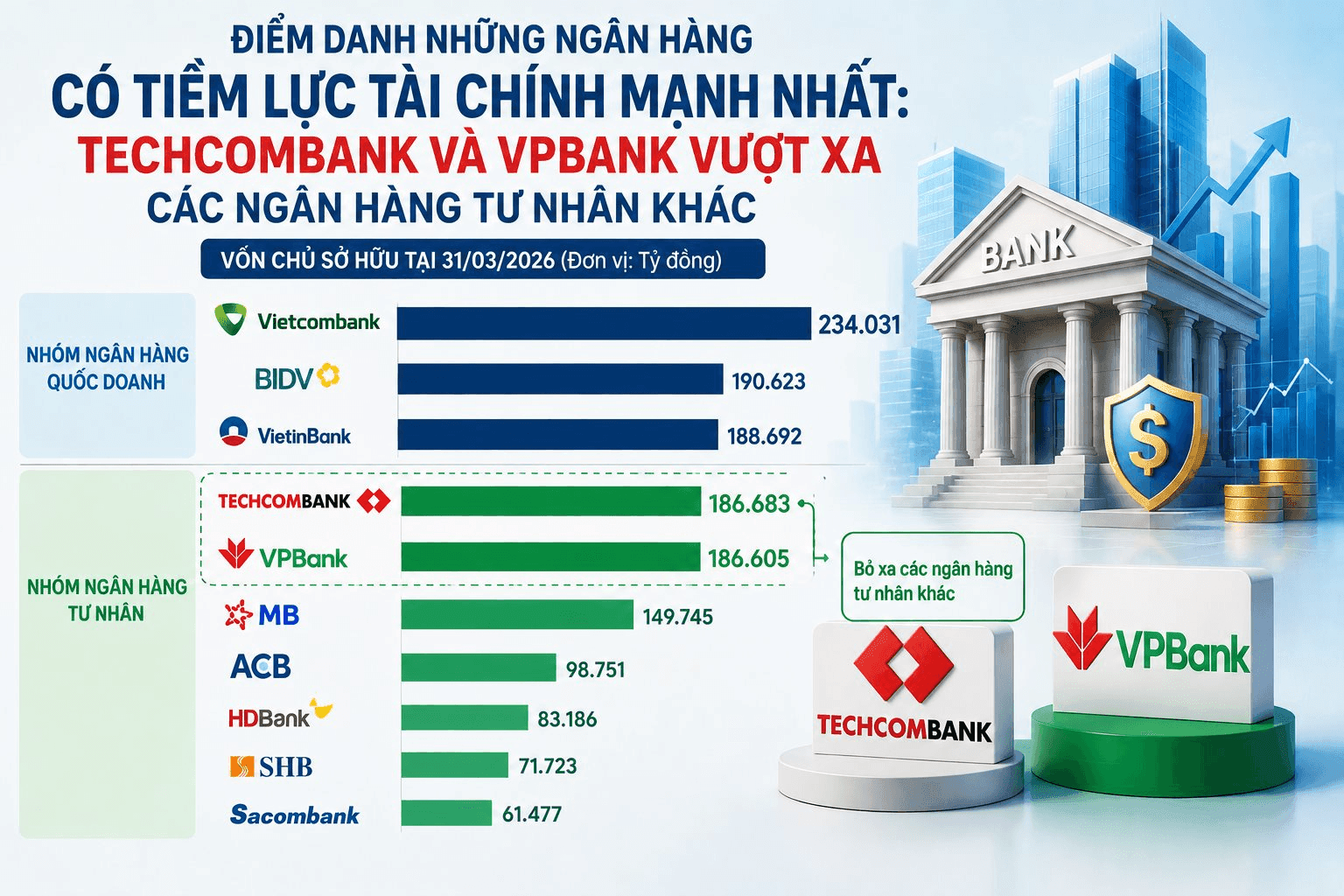

According to the consolidated financial statements for Q1 2026 of 27 listed banks, Vietcombank remains the bank with the largest equity in the system, at 234.031 trillion dong.

Right behind is BIDV with 190.623 trillion dong and VietinBank with 188.692 trillion dong. The gap between these two state-owned banks and the leading private banks group is relatively narrow.

Specifically, Techcombank reported equity of 186.683 trillion dong at the end of Q1 2026, about 2.0 trillion dong lower than VietinBank and around 4.0 trillion dong behind BIDV. Meanwhile, VPBank reached 186.605 trillion dong, close to Techcombank and tracking the two state-owned giants.

Beyond the top tier, the scale drops noticeably. MB posted equity of 149.745 trillion dong, about 37.0 trillion dong lower than Techcombank and VPBank. ACB recorded 98.751 trillion dong, roughly half of Techcombank or VPBank.

Other private banks such as HDBank and SHB recorded equity of 83.186 trillion dong and 71.723 trillion dong, respectively, by end-Q1 2026.

The figures highlight the disparity in financial strength within the private banking sector.

Notably, the pace of equity growth for Techcombank and VPBank is among the highest in the system. Compared with the same period last year, Techcombank’s equity rose by nearly 48.810 trillion dong, an increase of over 35%. VPBank grew by about 43.667 trillion dong, corresponding to more than 30%.

The drivers of capital growth for these banks mainly come from retaining most profits, paying stock dividends, and continuously expanding scale through M&A activities in recent years.

In contrast, smaller banks still maintain modest equity. Saigonbank currently has the system’s lowest equity at 4.267 trillion dong, while BVBank has 7.657 trillion dong and PGBank 8.081 trillion dong.

Equity is considered one of the key indicators reflecting a bank’s financial capacity. A larger capital base provides banks with more room to expand lending, invest in technology, strengthen resilience to risk, and meet increasingly stringent capital adequacy standards.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…