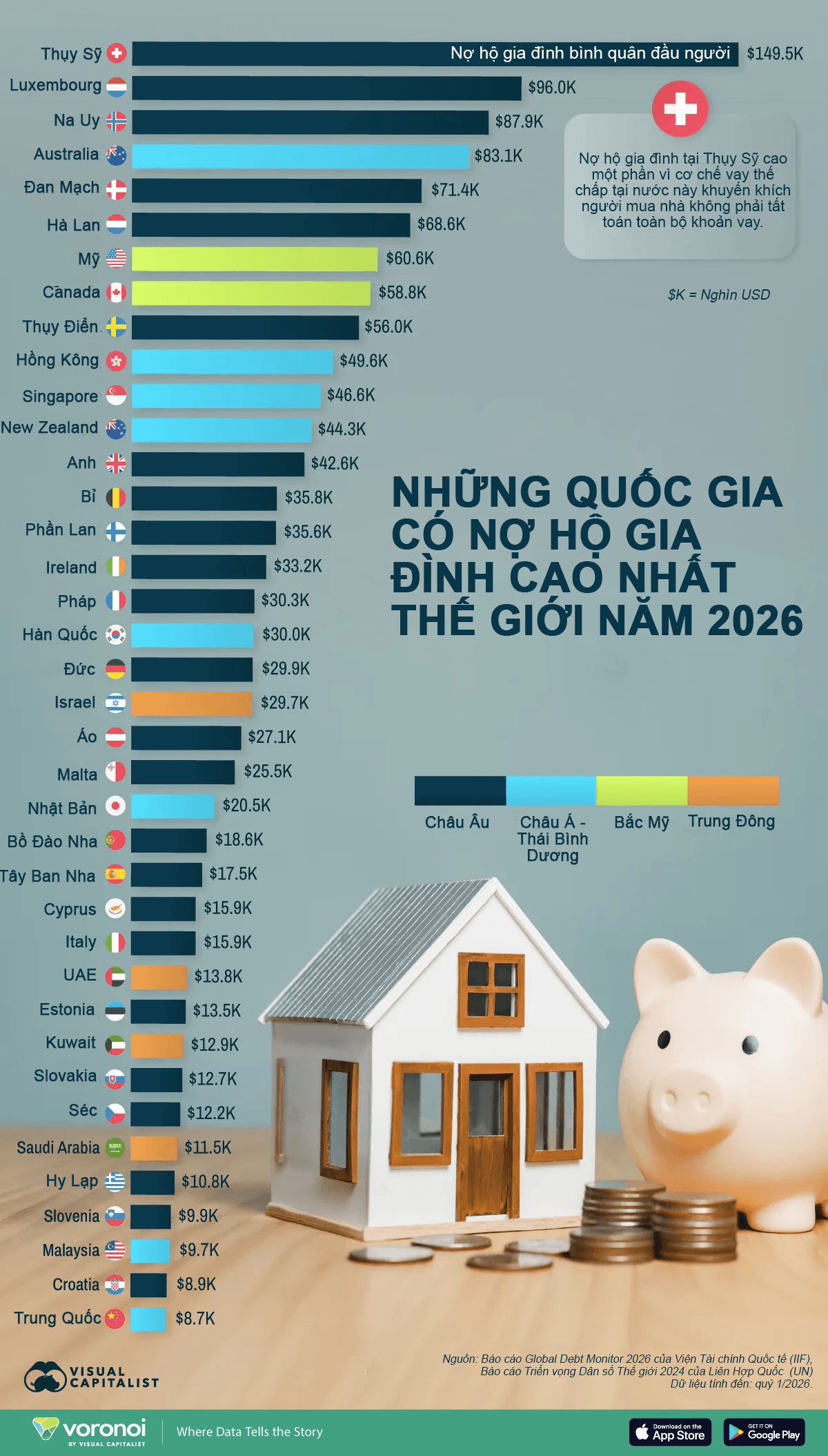

Household debt shows wide disparities across developed economies, largely due to differences in house prices, mortgage lending practices, and access to credit. Based on data from the Institute of International

Finance (IIF) and the United Nations (UN), the infographic below ranks economies by average per capita household debt in 2026. Switzerland ranks first worldwide in per capita household debt, at nearly $150,000 per person. This figure is much higher than other economies and more than twice the United States. However, high debt is not always a sign that households are financially strained. In many developed economies, high debt levels often stem from high housing prices, long-term mortgage borrowing to buy homes, and a developed credit market. In Switzerland, household debt is exceptionally high even among wealthy economies. An important reason is Switzerland's mortgage lending framework. Tax incentives and lending practices in the country tend to encourage homeowners to keep loans for a long time rather than repaying quickly as in many other places. Some of the world's most active housing markets are also among those with the highest per-capita household debt, including Australia at $83,100 per person, the United States at $60,600 per person, and Canada at $58,800 per person. Canada is notable as having the highest household debt-to-income ratio among the G7. By mid-2025, for every $1 of disposable income, Canadian households carried about $1.75 of debt. The United States ranks seventh globally in per-capita household debt. However, in absolute terms, the country has the largest total household debt in the world, reaching $21.2 trillion in Q1 2026. Much of this debt is driven by mortgage loans, while pressure is also rising in credit card and auto loan debt. The delinquency rate on mortgages in the United States remains near historical averages, but financial strains are more evident in other consumer credit segments. Between 2021 and 2025, delinquency rates on auto loans and credit cards rose sharply. Additionally, home foreclosure filings in the United States rose 26% in Q1 2026 from a year earlier, though still well below levels seen during the 2008 housing crisis. Home purchases have become more difficult as average mortgage payments have risen 44% since 2021. For new homebuyers, housing costs have increased by roughly $600 per month as a result. As housing costs continue to rise in many economies, household debt is increasingly a key component of modern economic structures. High debt levels can reflect high asset values, high homeownership rates, and a developed credit market. However, it also makes households more vulnerable to higher interest rates, slower economies, or falling housing prices.