•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

From an emerging markets (EM) perspective, Vietnam stands out for high profitability, though with relatively higher valuations. Vietnam’s return on equity (ROE) is currently the highest in the Asia EM region. In Q1 2026, listed companies continued to post strong growth: total revenue across all three exchanges rose 21.2% year over year, while net profit after tax attributable to parent shareholders (NPATMI) increased 35.2% YoY across the market and 49.8% YoY on HoSE.

The banking and real estate sectors remain the two main drivers of profit growth. Pre-tax profit of banks within SSI Research’s coverage rose 20% YoY, exceeding expectations by 10%. SSI Research attributed the outperformance primarily to CTG, TCB and MBB, supported by lower provisioning costs and/or improved non-interest income (NFI).

SSI Research data analysis indicates that credit continues to lead. Loan outstanding rose by about 20% YoY, lifting net interest income (NII) by 18%. The recovery in NFI, together with cost control increasing 10% YoY, continued to support overall profitability.

Credit is flowing along the real estate value chain. After an initial focus on lending to developers, credit is gradually shifting toward construction and project implementation. At the same time, demand for housing loans from end-users remains under pressure due to high interest rates.

Pressure on net interest margin (NIM) has eased. NIM returned to a lower level after falling to 3.04%, down 20 basis points QoQ and down 11 basis points YoY, driven by higher funding costs. Looking ahead, NIM is expected to remain a constraint on profit growth as funding costs stay high and there is limited room to optimize costs.

Asset quality weakened quarter-on-quarter but remained within control. The non-performing loan (NPL) ratio rose to 1.88% from 1.76% in 4Q2025, still below the 2.0% level in 1Q2025. A similar pattern is observed in the watch list (watch list 2). SSI Research described this as a familiar post–year-end balance sheet clean-up pattern, followed by normalization in 1Q and reflecting a lag in recognizing latent risk pressures.

The draft Circular replacing Circular 22 by the State Bank of Vietnam introduced several changes relevant to liquidity and capital metrics, including:

SSI Research assessed that these reforms are positive in the long run, helping the Vietnamese banking system move toward Basel III practices in the region while tightening liquidity discipline.

In the near term, the main risk is linked to the CDR. The cap of 85% remains during the 2028–2031 transition period unless banks achieve 100% LCR and NSFR, creating a hard overlay on capital metrics already calculated under different risk levels.

The impact of relaxing Treasury deposits is estimated to be modest—about +0.6% of total system loan demand. The impact is larger for state-owned banks, estimated at around +1.4% to 2.0%.

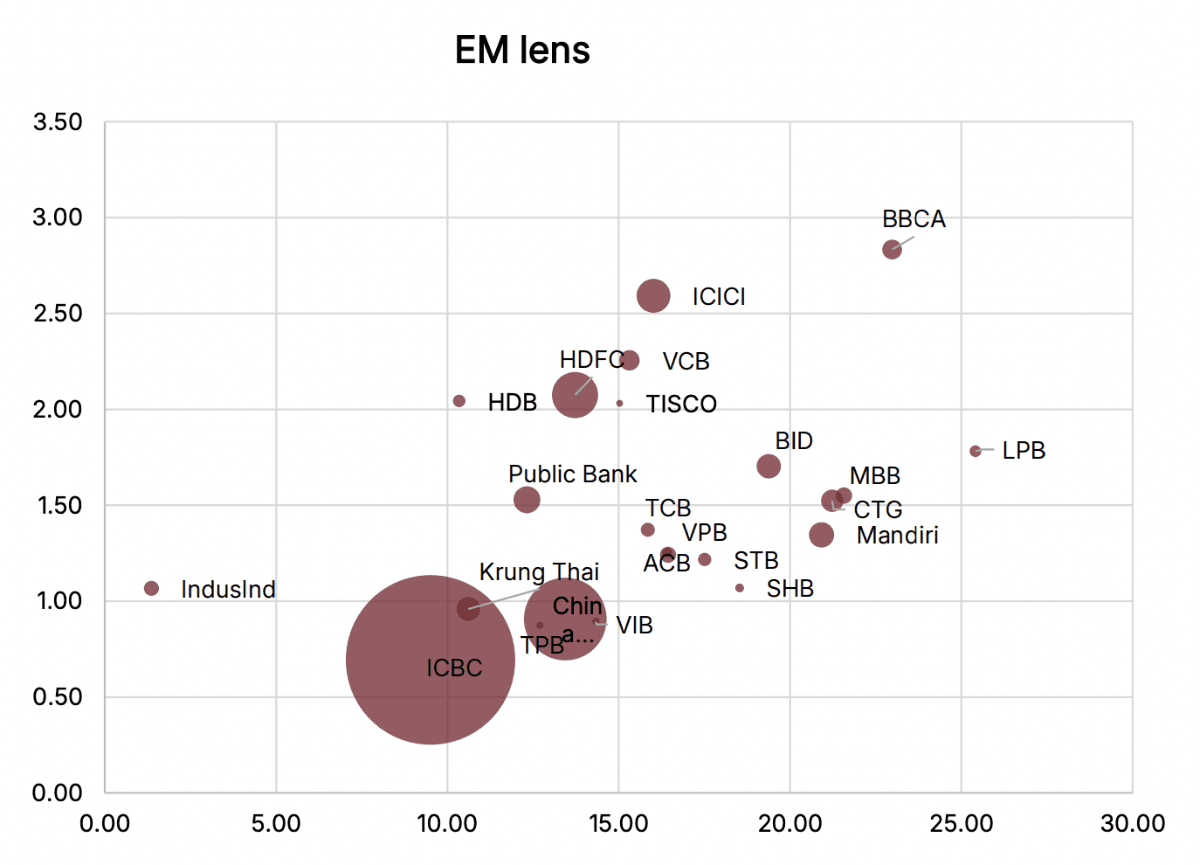

On valuations, SSI Research noted that Vietnamese banks stand out among EM markets. The base forecast remains unchanged as Q1 2026 results have completed about 23% of the current forecast. For 2026, pre-tax profit is expected to grow about 17% YoY, with ROE around 18%.

From an EM perspective, Vietnam’s ROE is the highest among Asia’s EM region at around 18%, with a price-to-book (P/B) ratio of about 1.7x. This is higher than India at 1.6x with ROE around 14% and Indonesia at 1.3x with ROE around 17%.

SSI Research said the higher valuation is supported by superior earnings growth, but remains capped by a high LDR around 105% and the lowest capital adequacy ratio (CAR) around 12.5% within the peer group. The analysis expects divergence to widen in a liquidity-tight and high-rate environment, with key determinants including the funding base, capital buffers, and disciplined risk governance.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…