•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

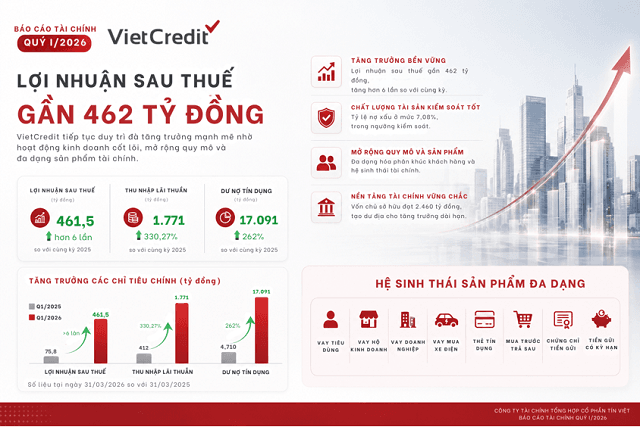

Q1 2026 financial statements show VietCredit continuing its strong growth trajectory, with net profit after tax reaching VND 461.5 billion, more than six times the year-ago period, reflecting improved asset quality, operating efficiency, and the durability of VietCredit's growth model. VietCredit, the consumer finance company (UPC0M: TIN), announced Q1 2026 results with several positive growth indicators, continuing the strong recovery since 2025. According to the disclosed financial report, VietCredit's Q1 2026 after-tax profit was VND 461.5 billion, up more than sixfold from VND 75.8 billion in the same period last year. This notable growth comes as the consumer finance market remains highly differentiated, forcing financial institutions to pursue growth, risk control, and operational efficiency simultaneously. Notably, profit in Q1 2026 did not come from non-operating items, but was driven mainly by core business activities, particularly a strong rise in net interest income. Net interest income rose 330.3% to VND 1,771 billion from VND 412 billion in Q1 2025. This was the main growth driver, reflecting improved efficiency in deploying assets to earn interest. Management commentary attributes this growth to continued strong loan growth, especially in digital lending products. As of 31 March 2026, VietCredit's total lending stood at VND 17,091 billion, up 262% YoY. Specifically, lending interest income in Q1 was about VND 1,576 billion, up 256.84% YoY. This trend indicates that VietCredit's profit growth is driven by core operations rather than non-operating income or one-off items. In a competitive consumer finance market, this signals the quality and durability of the growth in profits. Expansion of scale goes hand in hand with rising costs, but operating efficiency continues to improve. Alongside strong loan growth, VietCredit also recorded higher costs in Q1 due to scaling up. Specifically, net service income loss rose from VND 75.4 billion to 313.4 billion. Management cited operating costs and service fees paid to partners in the digital lending segment as the main reason, with costs in Q1 2026 totaling VND 305.6 billion, up 342.52% YoY. However, these costs are deliberate as VietCredit expands its digital lending ecosystem, reflecting the nature of the growth strategy. In other words, cost increases accompany higher disbursement volumes, not a decline in efficiency. On the operating side, total operating expenses in Q1 2026 were VND 97.6 billion, up 10.14% YoY. This rise mainly reflects personnel additions and investments in operating capabilities to meet the expanded scale. Compared with the growth rate of net interest income, the increase in operating costs remains modest, signaling improving efficiency. [Image showing VietCredit Q1 2026 financials] Increase in provisioning in line with scale; credit quality remains within control In Q1 2026, credit risk provisioning costs rose to VND 518.2 billion, higher than a year earlier. However, the increase still lagged the growth rate of credit outstanding. This matters because it shows the company actively setting aside provisions in line with credit growth while maintaining prudent coverage levels, with asset quality staying under reasonable control. As of 31/3/2026, VietCredit's NPL ratio stood at 7.08%, up modestly from the end of the prior year but still within the target range for the consumer lending portfolio. Certain segments show very low NPLs, such as household businesses (1.39%) and electric vehicle lending (near 0%). In a context where many consumer finance companies are still cleaning up legacy debt or slowing growth to manage risk, VietCredit’s simultaneous scale expansion and controlled NPLs indicate improving risk management and stronger growth quality. Expanding the multi-product digital finance ecosystem Beyond strong earnings, Q1 2026 also saw VietCredit expanding its digital finance ecosystem beyond lending to other attractive segments such as digital credit cards and BNPL, as well as capital raising activities. In lending, VietCredit continued to launch and expand several co-branded products with technology partners, such as Tin Vay on ZaloPay, Tin Vay PayDay (short-term small loans) with Zalo, and Tin Vay Biz for customers of FAST Accounting software. VietCredit also advanced Tin Vay Plus—an on-app consumer loan product integrated directly within the VietCredit app, targeting VietCredit’s ecosystem customers without relying on external partner platforms. Not limited to lending, VietCredit is also recognized for other financial segments such as digital credit cards, BNPL, and funding mobilization. The company plans to roll out a series of digital card products and BNPL models in the near future, signaling a multi-product, multi-touchpoint financial ecosystem expansion. On the funding side, VietCredit is implementing both offline and online products via term deposit certificates and term deposits for enterprises, organizations, and business households with competitive interest rates up to 9.9% per year. Strengthening the foundation for 2026 growth As of 31/3/2026, VietCredit’s total assets stood at VND 19,496 billion, up over 10.5% from end-2025. Equity reached VND 2,460 billion, while undistributed profits rose to nearly VND 1,493 billion, providing additional room for quarterly growth ahead. The Q1 2026 results show VietCredit entering a new growth phase with a more robust profit mix, driven more by core operations, with improved asset quality and operational efficiency. In the consumer finance sector’s ongoing restructuring, these results reflect positive momentum from a model moving toward digitization, better risk control, and longer-term sustainability.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…