•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Vietnam’s VN-Index closed at an all-time high based on the closing price, extending gains for a third consecutive session. The market’s near-term outlook remains constructive as momentum indicators continue to improve, with MACD widening versus the Signal line after a positive signal since late March 2026.

Trading across major indices was mixed. The VN-Index rose 0.94% to 1,909.01 points, while the HNX-Index fell 0.28% to 247.76 points.

On 07/05/2026, the VN-Index built on its positive momentum and moved above the 1,900-point level, supported by broad participation from large-cap stocks and improved liquidity. Momentum strengthened in the afternoon session, when the index reached a fresh intraday high of 1,924.95. However, profit-taking pressure at higher levels narrowed gains into the close, leaving the index at 1,909.01.

Large-cap stocks led the session. VS-LargeCap gained 1.01%, while VS-MidCap and VS-SmallCap declined 0.38% and 0.08%, respectively.

The 10 most influential stocks added 24.47 points to the VN-Index. VIC and VHM were the dominant drivers, contributing more than 17 points. STB, LPB, HDB and MSN followed, collectively adding about 5 points. On the downside, GAS and BSR each removed more than 1 point.

The VN30-Index finished up 25.69 points (+1.25%) at 2,079.1. Market breadth was mixed, with 13 gainers, 13 losers, and 4 unchanged. STB and VHM led the upside, while LPB, HDB and MSN rose more than 3%. On the downside, GAS, DGC and PLX faced selling pressure of over 3%.

Real estate was the standout sector, rising 2.51%. The move was anchored by VHM’s ceiling, along with VIC (+2.05%) and IDC (+2.44%). Several other real estate names declined, including NVL (-3.5%), DXG (-2.22%), CEO (-1.71%), KBC (-1.15%), TCH (-1.73%) and DIG (-1.69%).

Financials and industrials also supported the market. Demand appeared in stocks such as STB, GEE, GEX, HDB (+3.38%), MSB (+1.96%) and LPB (+3.64%). Meanwhile, declines were recorded in SHS (-1.71%), HCM (-0.88%), ACB (-0.87%), VCI (-2.26%), TPB (-1.23%), VCG (-3.66%), CII (-1.06%), PC1 (-3.79%), HHV (-2.71%), DPG (-3.26%) and CTD (-1.9%).

Energy and utilities were the weakest groups, falling 3.71% and 1.57%, respectively. The declines were led by BSR (-4.49%), PLX (-3.33%), PVS (-3.23%), OIL (-2.72%), PVD (-2.77%), PVP (-5.07%), GAS (-4.4%) and NT2 (-1.02%).

The VN-Index set a new all-time closing high for the third straight day. The near-term outlook is supported as MACD continues to widen from its Signal line after issuing a positive signal since late March 2026.

On HNX, the index fell after a choppy session, and trading volume stayed below the 20-session average, suggesting investors remained cautious. While MACD widened, it remained below zero, indicating higher near-term risk.

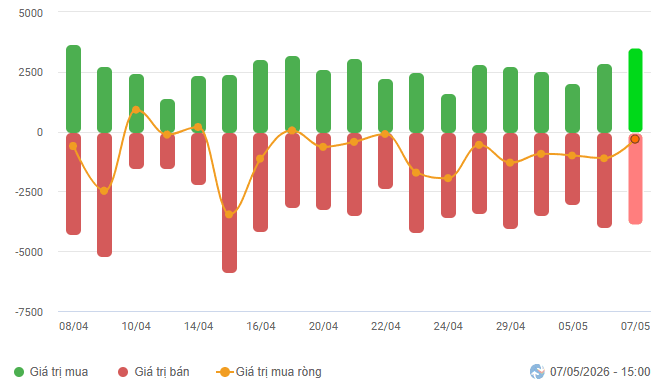

For the VN-Index, the Negative Volume Index is above the 20-day EMA. If this holds into the next session, the risk of a sudden downside thrust may be mitigated. In contrast, foreigners were net sellers on 07/05/2026; if this pattern continues, downside pressure could reappear.

[Images and references to market data, analysts, and related articles.]

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…