•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

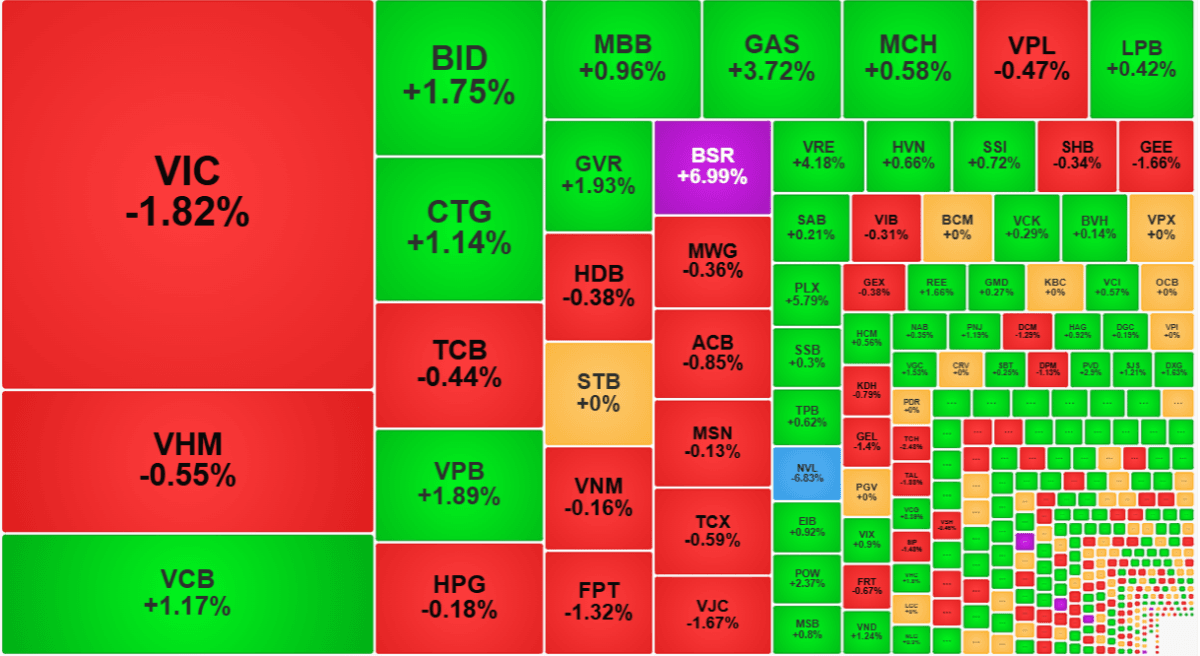

The VN-Index gave back almost all of its intraday gains, closing the morning session up just 0.08% (+1.56 points) after reaching an intraday high of up to 1.22% (+22.1 points). Sharp reversals in VIC and VHM weighed on the index, though positive market breadth suggested buying interest persisted in other stocks.

VIC closed the morning session down 1.82%, sliding as much as -4.5% from the day’s early peak. VHM also fell, dropping as much as -2.55% and currently down -0.55% versus the reference. VPL fell -0.47% and saw an in-session high-to-low swing of up to -2.07%. Together, the two Vin group stocks contributed to the VN-Index losing nearly 7 points.

Despite the reversals, liquidity for VIC and VHM was weak. VIC matched 402.3 billion dong, down 25% from the pre-holiday session, while VHM matched 261.5 billion dong, down 48%. The article attributes the reversals to “problematic” buying demand rather than heavy selling. It also notes that both blue chips reversed again on April 29 with much higher liquidity, suggesting buying power may have become “stuck.” VHM has not yet reached a new all-time high, while VIC has shown strong sell signals over the past five sessions.

Price declines were not limited to VIC and VHM. The entire VN30 basket declined to varying degrees, with 17 codes down more than 1% from the day’s peak. The VN30-Index, which had risen 0.84%, reversed to a -0.21% loss. Within the group, breadth shifted from initially 1 stock down and 1 flat to 14 up and 15 down before the noontime break.

Liquidity across VN30 was also described as weak, accounting for only 49.3% of the total value matched on HoSE—its lowest liquidity share in 10 sessions. By contrast, liquidity in mid- and small-cap stocks remained solid. HoSE turnover rose about 8.1% versus the previous session, adding roughly 667 billion dong in absolute terms, while the VN30 basket rose by 193 billion dong.

Representative indices such as Midcap (+0.36%) and Smallcap (+0.24%) did not diverge sharply from the blue-chip group. However, overall HoSE breadth improved to 179 gainers versus 119 decliners, indicating relatively good price retention outside VN30. The best breadth on the exchange reached 211 gainers to 71 decliners around 9:47, and the number of stocks trading below reference did not become excessive.

On the upside, 82 HoSE stocks rose more than 1%, with VN30 contributing 8 gainers. Notable gainers included GAS (+3.72%), VRE (+4.18%), and PLX (+5.79%). The mid- and small-cap segment also saw dozens of stocks rise more than 2% up to the daily limit. BSR, C32, DXS, and ASM hit the daily limit. Other cited gainers with relatively high liquidity included BFC (+4.88%), VCG (+3.39%), PVD (+2.9%), PC1 (+2.81%), BMP (+2.68%), and HSG (+2.45%). The 82 strongest stocks accounted for around 31% of total HoSE matched value.

Because early breadth was solid and prices moved upward before pulling back, the article says relatively few stocks dropped more than 1%. Among 119 red stocks, only 50 fell more than 1%, and only 11 of those had liquidity above 10 billion. NVL was highlighted for an abrupt sell-off between around 9:40 and 10:00, with the price sliding to the floor while still showing more than 13.1 million shares on offer. The article links the move to NVL’s more than 95% rally since March 10 and notes it led market liquidity with nearly 679.5 billion dong, equivalent to about 34.7 million shares sold.

Foreign investors were net sellers of about 616.6 billion dong on HoSE. The article describes the selling as broad-based rather than a one-off spike. Leading net sellers included HPG (-154.7 billion), FPT (-137.7 billion), VCB (-85.4 billion), ACB (-73.2 billion), MWG (-51.2 billion), and NVL (-44.9 billion). On the buy side, VRE (+48 billion), VCG (+34.5 billion), and BSR (+30.8 billion) were cited.

With volatility concentrated in blue chips, the VN-Index is hovering around the late-February 2026 peak. The article frames the continued attraction of mid- and small-cap stocks and the market’s ability to maintain leadership differentiation as a positive signal, suggesting investors are still finding opportunities even as the index level does not move in tandem with most stocks.

Bitcoin (BTC) investors who use steady dollar-cost averaging (DCA) may be underperforming versus strategies that adjust exposure to the market’s cycle, according to new research arguing that Bitcoin’s behavior differs from traditional long-duration assets.

In a report cited by Markus Thielen of 10x Research, Bitcoin’s market…