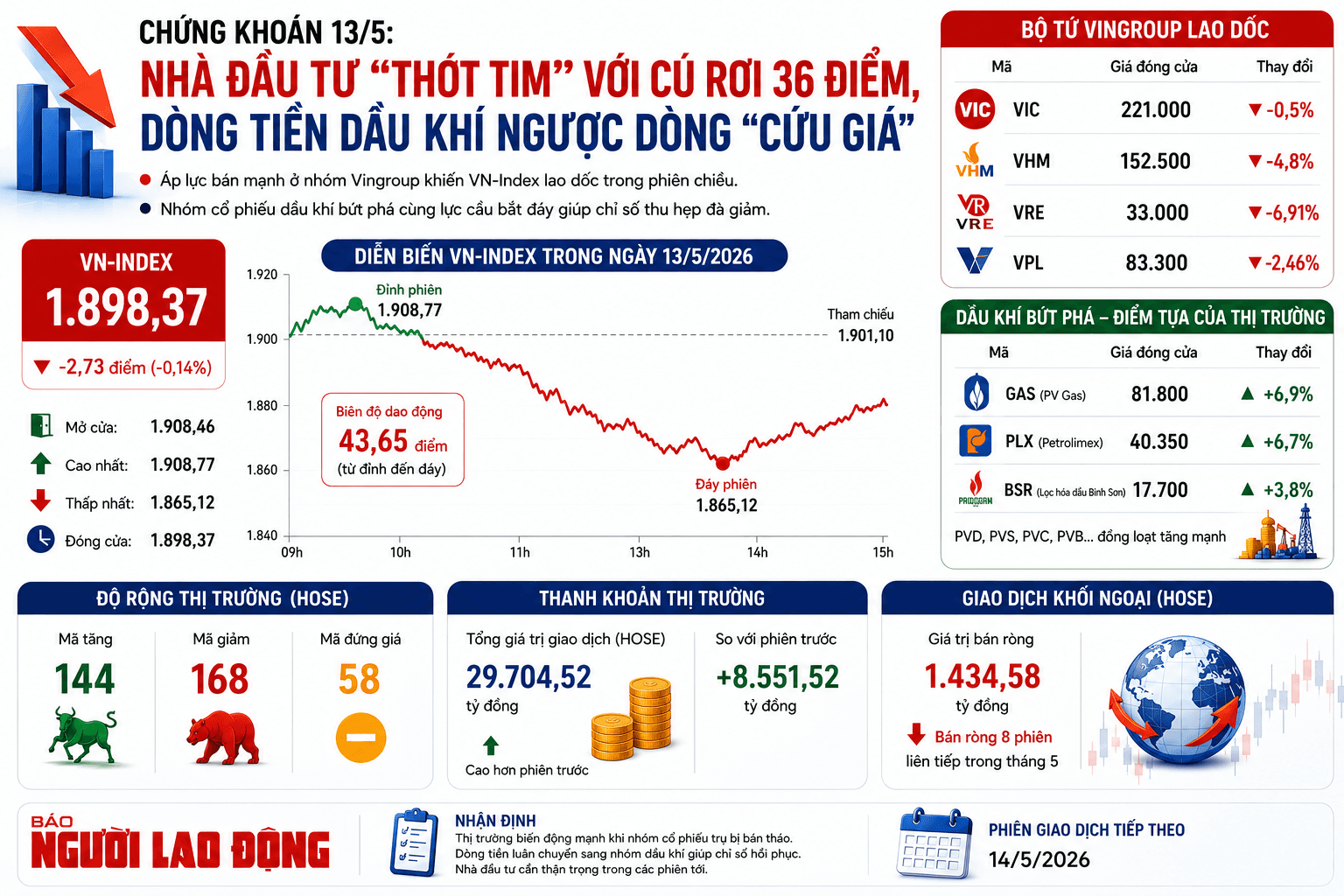

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Brokerage firms are recommending different stances on three Vietnamese stocks—BSR, EIB and REE—citing diverging views on refining margins, bank profitability recovery, and near-term earnings risks versus longer-term growth drivers.

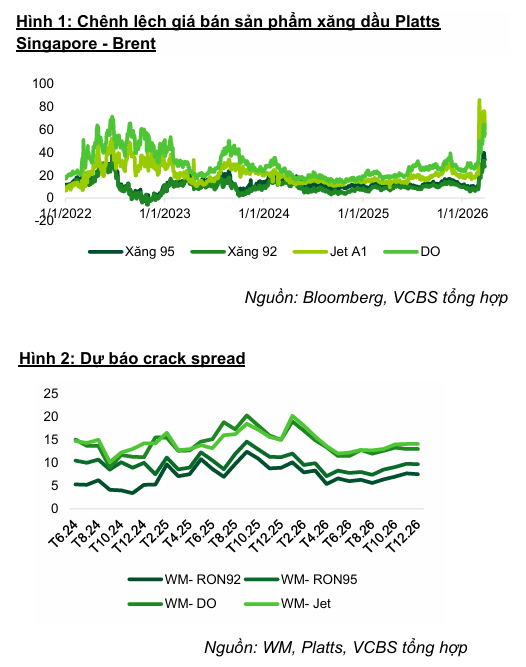

VCBS recommends buying BSR (Binh Son Refining and Petrochemical) with a target price of 34,533 VND per share, supported by widening gasoline and diesel crack spreads and growing demand for fuel products.

For the first quarter of 2026, VCBS expects cumulative production and sales by 15/03 to reach 1.67 million tons, equivalent to 21% of the annual plan. VCBS projects revenue of 32 trillion VND and pre-tax profit of 2.1 trillion VND.

Crack spreads for gasoline and diesel products are estimated to have risen 50%–115% year-on-year, driven by geopolitical tensions and supply disruptions in the Middle East.

Based on materials from BSR’s 2026 annual general meeting, the company maintains a high production and consumption plan: production of around 7.76 million tons and consumption of around 7.71 million tons. Diesel is targeted at above 3.5 million tons, RON95 gasoline at around 2.38 million tons, and Jet A1 at nearly 0.6 million tons.

Combined revenue is expected at 154,140 billion VND, with net profit after tax at 2,162 billion VND.

Since the latest report dated 22/01, BSR’s stock price has risen by more than 50%. VCBS maintained a positive view on the 2026 profit outlook, citing widened refining margins amid supply disruptions, and raised its target price by an additional 35% to 34,533 VND per share, implying about 31% upside versus the current price.

VCBS also presented a more optimistic scenario assuming plants operate at 123% of design capacity for 2026, targeting 40,102 VND per share.

For EIB (Vietnam Import-Export Bank), VCBS recommends increasing weight with a target price of 26,000 VND per share.

Mirae Asset (Vietnam) said EIB’s 2025 results were pressured by narrowing net interest margin (NIM), lower fee income, and a sharp rise in provisioning costs. ROE fell to 4.4% and ROA to 0.44%, while total operating income declined 14.8%.

NIM narrowed by 33 bps to 2.48% as funding costs rose 42 bps to 4.22%, outpacing a 16 bps rise in lending yields, resulting in net interest income (NII) growing only 0.9% year-on-year.

The cost-to-income ratio (CIR) rose to 58.3% due to a 25.1% increase in operating expenses (OPEX) while revenue declined.

Asset quality indicators deteriorated: NPL (3–5) rose to 2.9% (up 34 bps) and the bad loans ratio (2–5) widened to 4.1% (up 52 bps). Loan loss reserve coverage was 43.9%, below the industry level, while provisioning costs rose 57.5%. Mirae Asset expects provisioning costs to remain high in 2026.

On liquidity and capital, loan growth reached 11.3%, above dynamic growth of 5.9%. CASA was around 14.1% (down 62 bps), continuing to decline and pressuring funding costs.

Mirae Asset said the dual pressure from funding costs and balance sheet adjustments pushed 2025 profits to a bottom, setting a base for recovery in 2026. It expects EIB’s performance to improve as a turning point under new leadership from Gelex, with growth anticipated through expanding its ecosystem.

Mirae Asset recommended increasing EIB weight with a target price of 26,000 VND per share (2026 P/B around 1.7x), based on RI and P/B valuation.

For REE, SSI takes a neutral view despite long-term growth drivers from renewable energy. SSI maintains a 12-month target price of 70,200 VND per share, implying about 6% upside.

SSI’s investment theses are twofold: REE continues expanding its power segment toward roughly 3GW by 2030 (from around 1.2GW currently), with renewable energy as the core long-term driver; and stable growth across core M&E and office leasing segments supported by a healthy backlog and improving occupancy at E.town 6.

However, SSI remains cautious because office leasing faces near-term pressure from increased supply, while leasing demand is recovering slowly.

Based on REE’s 2026 AGM content, the company set a net profit growth target for 2026 of 11% year-on-year, versus SSI’s previous forecast of a 4% decline. SSI said the discrepancy largely reflects El Niño effects on hydro output and the expected recognition of remaining units at Light Square in 2026.

SSI’s cautious stance is also tied to recent weather data.

SSI projects 2026 revenue of 10.9 trillion VND (up 9%) and net profit of 2.4 trillion VND (down 4%).

The forecast is based on two key assumptions: hydro output cycles affecting production and efficiency, and remaining Light Square apartments being recognized mainly in 2027 rather than 2026 as the company had planned.

REE is considering temporarily suspending stock dividends in 2026 to minimize EPS dilution after five consecutive years of such distributions at around 15% annually.

SSI noted risks including plant operation issues and short-term occupancy pressures in office leasing that could affect rental income.

SSI said its neutral stance is based on a valuation approach combining P/E and sum-of-the-parts to reflect long-term growth potential against near-term earnings pressure.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…