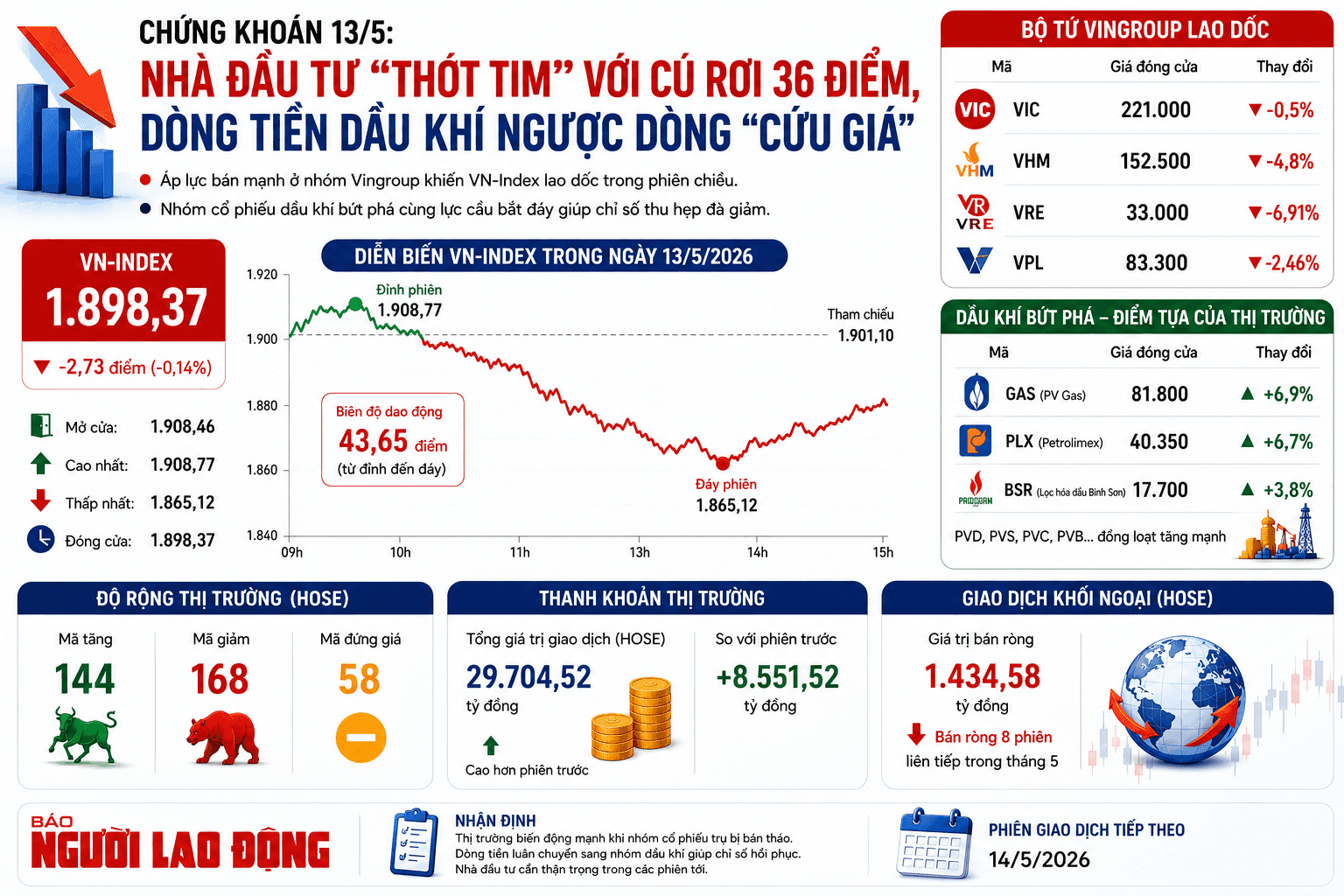

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Vietnam’s stock market is experiencing its longest stretch of foreign net selling since October last year. After 14 consecutive sessions of selling on HoSE, foreign investors have net-sold more than 13 trillion dong via the order-matching channel. Foreign net selling has persisted for months across Vietnam’s equity market.

Last year, net selling on HoSE reached a record of over 125 trillion dong. From the start of the year to date, there has not been a single month with foreign net buying; the year-to-date total is nearly 53 trillion dong.

A key point is that foreign capital continues to retreat even after FTSE upgraded Vietnam to secondary emerging market status on April 8. Since then, foreigners have net-sold through HoSE’s order-matching by nearly 12 trillion dong.

The selling trend may reflect both time-specific factors and market-structure issues. The upgrade to emerging market status could prompt some frontier-market funds to withdraw. In addition, a stronger U.S. dollar amid Middle East tensions has created FX pressure, which can affect short-term foreign flows.

Another long-standing challenge for Vietnam’s market has been difficulty in fully unlocking new supply. While there have been some IPOs, they remain concentrated in traditional sectors. The market structure is still imbalanced, with financials and real estate continuing to dominate. Concentration risk is also a concern, as the weights of certain stock groups within ecosystems are large enough to influence index performance.

Despite the near-term outflows, the upgrade narrative is expected to support foreign capital inflows back into Vietnamese equities over the longer term.

According to David Rabinowitz, Global Indices and Asia-Pacific Market Structure Analysis Director at UBS, the upgrade process is expected to unfold in multiple stages, with weight increases of around 30% at each stage. He noted that the market needs time for practical implementation to ensure it meets all criteria, and that the process may be lengthy because it is the result of more than a decade of ongoing reforms.

If the current improvement trajectory is maintained, Vietnam could evolve from a niche market into a more significant destination for international capital.

Earlier this month, FTSE Russell adjusted Vietnam’s weight in global indices based on data as of March 31, 2026. Vietnam’s weight in FTSE Emerging All Cap declined from 0.350% to 0.329%, while its weight in FTSE All-World fell from 0.024% to 0.020%. The weight in FTSE Emerging also decreased from 0.227% to 0.192%.

SSI Research, using estimates drawn from FTSE-indexed ETFs, suggests total possible inflows into Vietnam could reach about $1.3 billion. Large funds such as Vanguard Total International Stock ETF and Vanguard FTSE Emerging Markets ETF are expected to contribute significantly.

Vietnam is also working to meet MSCI criteria. SSI Research further points to the possibility that Vietnam will be added to the MSCI Watchlist in June 2026 as underlying drivers converge.

SSI Research says Vietnam currently meets most MSCI criteria for market accessibility, supported by the stabilizing operation of the pre-trade no-funds (NPF) framework, progress in implementing a central counterparty (CCP) clearing model, and the expansion of hedging and short-selling tools via index futures. It also cites markedly improved English-language disclosure and ongoing improvements in foreign ownership limits (FOL).

Notably, the market-wide FOL ratio—especially on HOSE—has improved significantly in 2025 to early 2026 due to the entry of large-cap stocks with 100% foreign room. SSI Research says this broadens the pool of investable stocks for index funds and improves representation and depth of markets in global baskets.

Remaining challenges mainly relate to liberalization of the foreign exchange market, an important criterion in MSCI’s framework. The report adds: “However, this is not a bottleneck at this stage, given that many other emerging markets in MSCI also do not meet ideal FX and capital-flow conditions.”

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…