•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

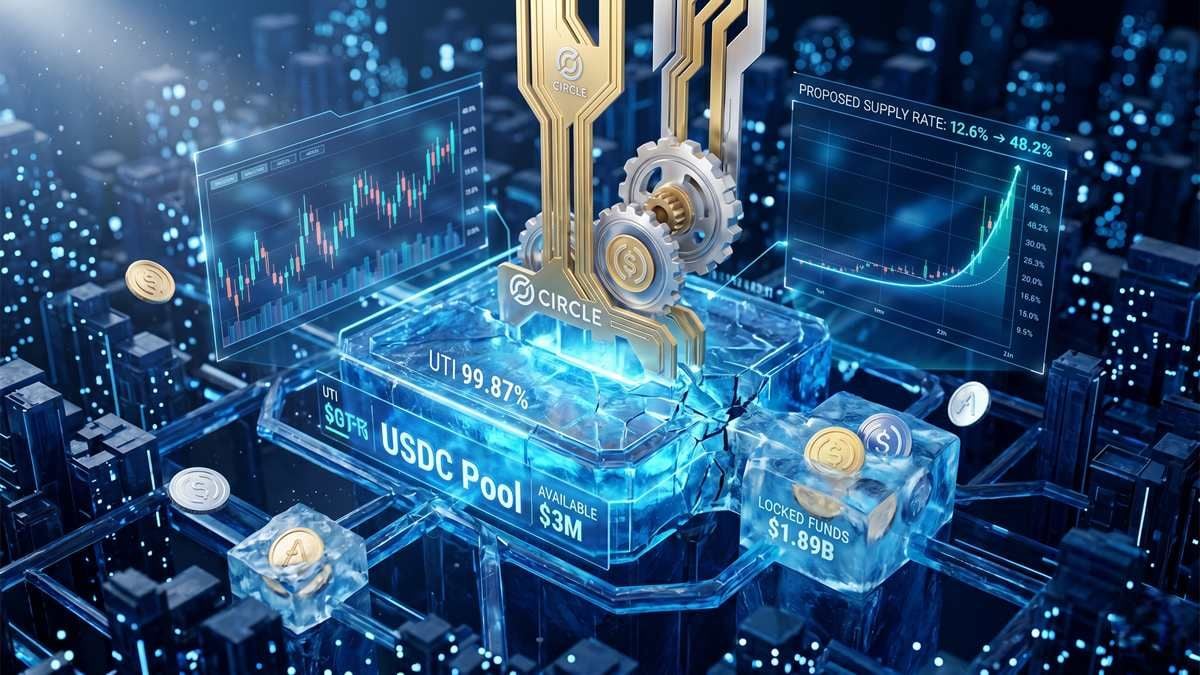

The utilization of the USDC pool in Aave V3 on Ethereum has reached 99.87%, leaving barely $3 million in available liquidity, according to a proposal discussed by Gordon Liao, an economist at Circle. Liao’s plan would raise the maximum interest rate from 12.6% to 48.2% to incentivize large deposits quickly and restore normal withdrawal conditions.

Under the new scheme, the optimal utilization of the pool would be reduced from 92% to 85% after official ratification. The proposal also targets a major increase in the maximum supply rate: if utilization reaches 100%, the annual interest rate would scale from 12.6% to 48.2%.

Liao argues that the current borrower base is “rate-insensitive” and is using the pool as an exit mechanism for trapped positions. In that context, he says a supply shock is needed to rebalance liquidity.

In addition to changing interest parameters, the proposal calls for pausing Aave’s “Slope 2 Risk Oracle” for the USDC asset. Circle cites poor performance of this oracle during previous volatility spikes and notes the recent disengagement of Chaos Labs as system maintainer on April 6.

The proposal is described as unusual for DeFi because it involves an institutional asset issuer directly intervening in the governance of a decentralized protocol. Circle maintains that the market for its asset is technically “broken” and requires shock measures to prevent a major collapse.

Circle expects yields in the 40% to 50% range to attract fresh capital from large allocators within a few hours. The incoming liquidity would be used to normalize the utilization rate and enable users with locked funds to make withdrawals without current restrictions.

The proposal is framed as a way to unlock nearly $2 billion in USDC within Aave. It follows the KelpDAO exploit on April 18, which caused an operational freeze affecting $1.89 billion in supply.

If approved, Circle’s approach would set a precedent for how stablecoin issuers manage liquidity crises in secondary lending markets.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…