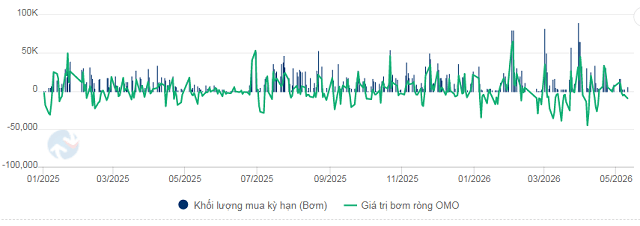

During the first week of May (04-11/05), the State Bank of Vietnam (SBV) shifted to net draining on the open market, while the banking system showed no material liquidity pressure, reflected in declines in interbank rates across several tenors.

SBV injected 49,000 billion VND through open market operations (OMO) for tenors of 7-56 days at an annual rate of 4.5%. At the same time, the amount maturing on the collateralized lending channel reached nearly 53,042 billion VND.

As a result, SBV net drained about 4,042 billion VND in the week, bringing the amount of OMO in circulation to 266,548 billion VND.

On the interbank market, rates cooled versus late April across multiple tenors. The 1- and 2-week tenors declined by 86 and 58 basis points to 5.37% and 5.90% per year, respectively. The 1-month tenor also fell by 77 basis points to 5.94% per year.

By contrast, the overnight rate rose the most, increasing by 111 basis points to 4.99% per year. The 3-month tenor rose by 45 basis points to 7.53% per year.

In the foreign exchange market, the USD Index (DXY) fell 0.58 points to 97.78 as of the end of the week (08/05), the lowest in 10 weeks. The decline was linked to cooling demand for the USD as a safe-haven asset, as gains in the S&P 500 moderated.

Separately, the University of Michigan consumer sentiment index fell to 48.2 in May from 49.8 in April.

U.S. economic data released during the week delivered mixed signals for the USD. Nonfarm payrolls rose by 115,000, above expectations of 65,000. However, average hourly earnings growth lagged expectations, reinforcing expectations that the Federal Reserve will maintain a cautious policy stance in the near term.

Domestically, exchange rates at commercial banks moved in line with international trends and remained below the ceiling. By the end of the week (08/05), Vietcombank quoted the USD at 26,087-26,367 VND/USD (buy-sell), down 21 VND on the buy side and down 1 VND on the sell side compared with the previous week.