On June 22, 2026, the State Bank of Vietnam issued Circular 25/2026/TT-NHNN, effective July 1, 2026. MASVN analysts say this is among the most notable liquidity risk management adjustments since 2019. The circular introduces two core changes: raising the cap on short-term funding for mid- and long-term lending (SFL) from 30% to 40%, and revising the calculation of the loan-to-deposit ratio (LDR).

The changes reflect a policy shift to support medium- and long-term credit growth in an economy that needs long-horizon investment funding. The move comes as Vietnam prepares to implement Basel III standards through four new indicators (LCR, NSFR, LEV, and CDR). MASVN notes that the system remains under pressure while the SBV transitions toward Basel III requirements. NSFR is expected to replace the SFL cap from 2028, making the 40% cap a near-term easing to support growth before tighter liquidity discipline takes effect.

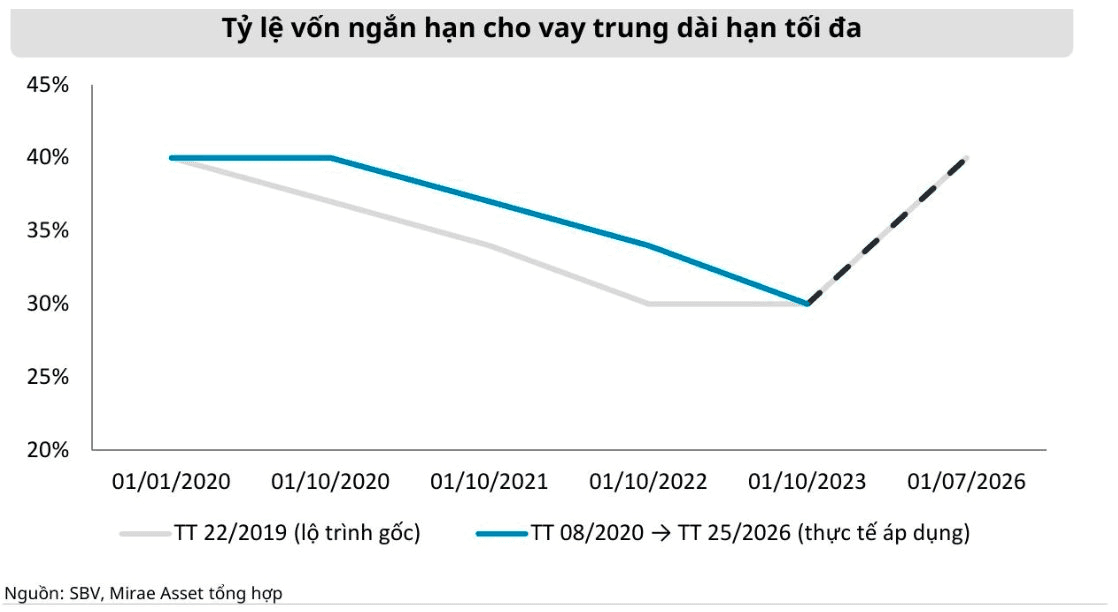

The SFL cap is raised to 40% from 30%. This reverses the gradual tightening since 2019, when the cap was reduced through Circulars 22/2019 and 08/2020 from 40% to 37%, then 34%, and finally 30% from October 2023. The higher cap is intended to support medium- and long-term credit growth by providing banks with cheaper short-term funds for longer-dated assets, reducing pressure to secure long-term deposits or issue high-yield instruments and helping to support net interest margins and lending costs in key segments.

The circular continues to exclude non-term deposits of the State Treasury from the LDR denominator and allows excluding 80% of the State Treasury's time deposits. This is a technical adjustment with real implications for banks holding large budget deposits—primarily state-owned commercial banks—lightening the denominator and improving reported ratios without altering the funding structure. Circular 25 repeals Circular 08/2020/TT-NHNN and Circular 08/2026/TT-NHNN, replacing the previous liquidity risk framework.

Reported LDR figures for listed banks are cited by sources such as Fiinpro and Mirae Asset. The reform anchors the move toward Basel III, with NSFR set to replace the SFL cap from 2028.

By enabling cheaper short-term funds to finance loans longer than 12 months, the change reduces the pressure to chase long-term deposits or issue high-yield instruments. The fall in competition for deposits can help lower funding costs and support net interest margins (NIM), easing lending costs in key segments. MASVN cautions about risks from increased maturity mismatch when long-term assets are funded with short-term funds, the very concern that motivated tightenings in 2019–2023.

Beneficiaries include state-owned banks (VCB, BID, CTG), which can gain from both the SFL expansion and LDR improvement. Private banks with high CASA ratios like TCB and MBB are expected to leverage the cap to widen net interest margins, with TCB most exposed due to nearing the SFL cap and large real estate loan books. Retail banks relying on deposits and consumer housing loans (VPB, HDB, TPB) may also benefit through margin protection amid funding costs. More conservative banks or those restructuring (ACB, STB, LPB, SHB) are less dependent on SFL room but still benefit indirectly as overall funding costs ease.

MASVN notes that while the system remains under pressure, the 40% SFL cap provides near-term support for growth ahead of Basel III liquidity discipline. The adjustment is viewed as a measured step to ease funding costs and support lending, with attention to the risks of maturity mismatch as long-term assets are funded with short-term funds.