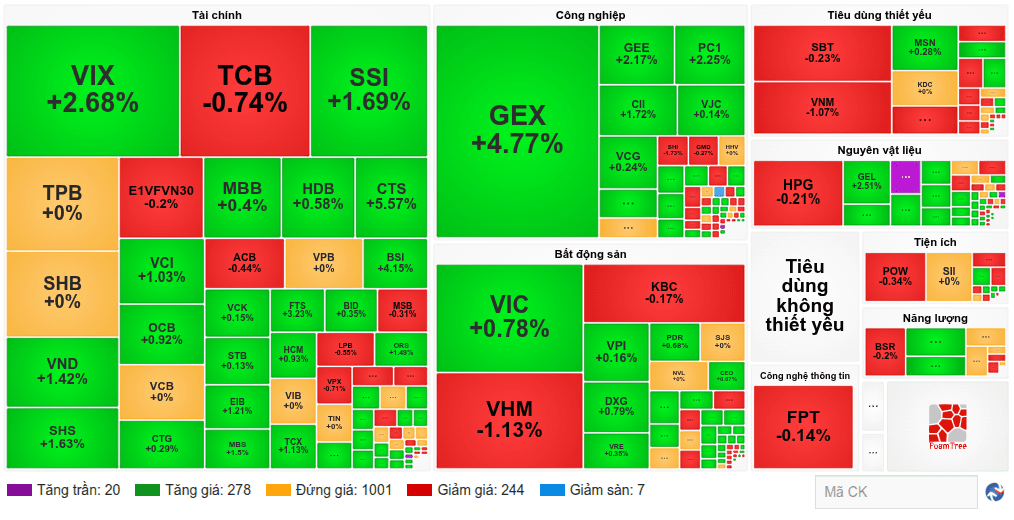

At the close of the morning session, the VN-Index rose modestly by 3.5 points to 1,858, while the HNX-Index declined by about 3 points to around 315. Market liquidity stood at about 7.6 trillion dong, roughly in line with recent sessions but still below earlier highs.

Opening: Heavyweight stocks exerted pressure at the start, keeping the opening level modestly down despite a buyer-skew. By 9:25 am, market breadth showed nearly 240 gainers against more than 140 losers, with green spread across financials, materials, and industrials. In the financials sector, gainers included CTS, VIX, OCB, SHS, MBS, among others. In the industrials group, GEX, GEE, PC1, and CTD rose modestly, while declines occurred in VCG, VJC, GMD, and C69. In materials, GEL, GVR, PHR, DCM, DPM, and DGC rose, with TRC recording a limit-up move. Heavyweight stocks continued to exert a gentle drag on the index, with VHM, VIC, VRE, and KBC edging lower. The VIC/Vingroup influence helped keep the index hovering around the reference, while VHM dragged about 1.5 points. On the HNX, THD fell, pulling the index below the reference.

Across the morning, the market tilted toward buyers but the gains were uneven. The 10:30 update showed the VN-Index up more than 3 points while the HNX-Index fell by 3 points. By 10:40 am, the market moved into a dispersion phase with breadth widening as decliners rose notably versus the opening, and green and red interspersed across nearly all sectors. The securities group stood out as the morning’s star, with most stocks rising; CTS surged more than 5%. Among the top movers, SSI, VIX, and TCX contributed more than half a point to the index. The index’s gains were driven by contributions from VIC and MCH, while VHM dragged about 1.5 points. GEX rose nearly 5 points in the morning session, recording the highest liquidity in the industrials group. Overall, financials and industrials were the most positive sectors, while information technology and consumer staples names were more mixed.

The gains in VIC helped lift the VN-Index by about 3.3 points, while VHM’s decline shaved roughly 0.6 points off the index. The strong morning performance of financials, industrials, and real estate provided overall positive contribution, with securities stocks performing better within financials and with 1% gain in VIC providing a major uplift on a point basis.

Market participants remained cautious as liquidity stayed limited and did not improve significantly. While some sectors showed positive momentum—particularly financials and industrials—the breadth of the market was uneven, and broad gains were not sustained beyond the morning session.