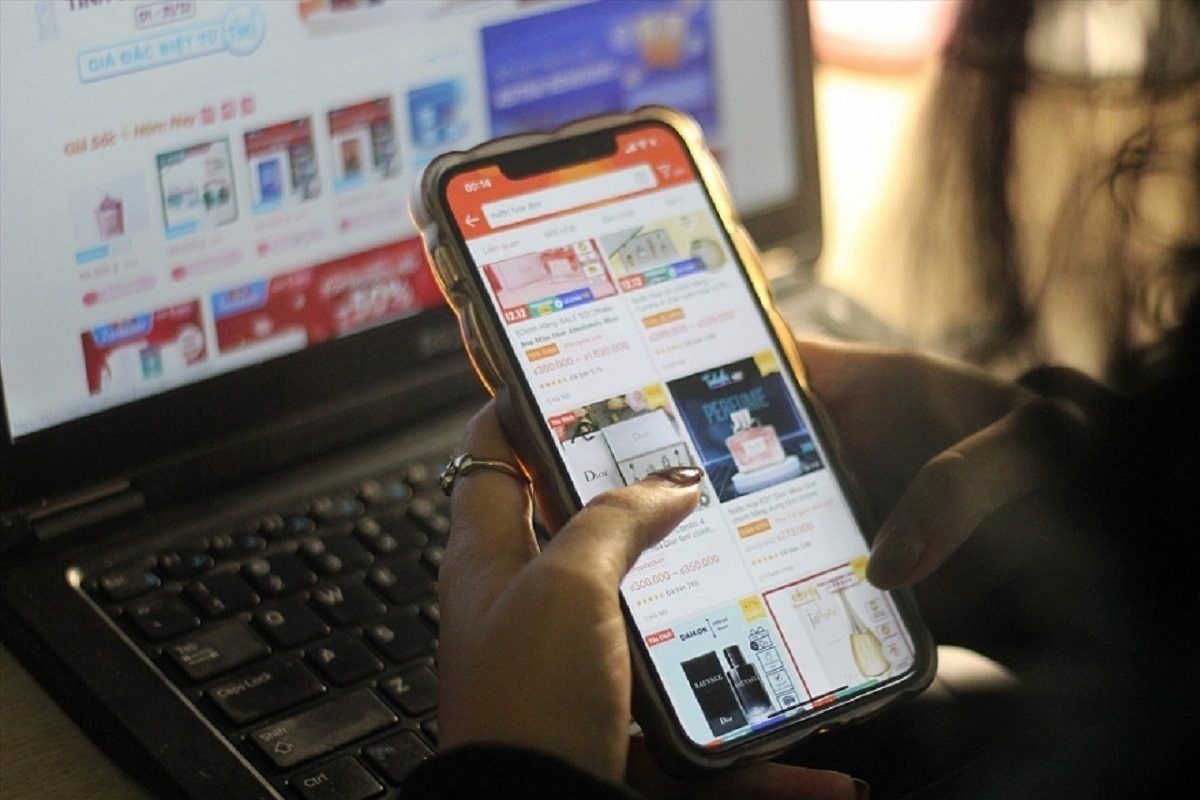

Online shopping is no longer just about bargains for consumers. In 2025, the four platforms Shopee, TikTok Shop, Tiki, and Lazada reported a total merchandise value (GMV) of 458.16 quadrillion VND, up 26% year over year, well above the 9.2% growth in the broader retail sector for goods and services. On the surface, Vietnam’s e-commerce market appears to continue growing rapidly, but a closer look reveals a notable signal behind the revenue surge: in Q4 2025, platform sales volume fell by 8% year over year, while the average selling price across the four platforms rose by 33% from Q4 2024. YouNet ECI attributes this price rise to a series of platform-fee increases in 2025. In other words, e-commerce is still growing, but not in the same way as before. Consumers are spending more on platforms, but not necessarily buying more items. Growth is increasingly driven by higher prices rather than higher product volumes. Fees charged to sellers include transaction fees, fixed fees, payment fees, vouchers, participation in promotional programs, affiliate fees, and advertising costs. When these costs rise over time, sellers cannot bear the burden alone. Theoretically, a shop has three options: keep prices and accept thinner margins, raise prices to cover costs, or exit the platform if margins are no longer viable. For small sellers with thin margins, option one becomes harder. Maintaining price competitiveness can preserve orders but may turn each order into a small loss. Thus, as platform fees rise, the cost is not confined to the seller. It tends to be passed into the selling price, into shallower discounts, into less generous voucher terms, or into stricter free-shipping conditions. Consumers may think they are outside the platform-fee battle, but they ultimately pay the bill. This explains why shopping activity on platforms remains vibrant, but the sense of getting a bargain diminishes. Livestreams continue, banners proliferate, double-day campaigns are intensified. If the base price has already been stepped up to offset costs, discounts may only temper the increase rather than return buyers to earlier cheap-price levels. Consumers are starting to respond with their wallets. The Q4 2025 data show not only that prices are higher, but that behavior has shifted. An 8% drop in throughput during the same period, alongside a 33% price increase, suggests buyers are more cautious with their online wallets, browsing more thoroughly, waiting for deeper codes, trimming non-essential purchases, or shifting to items with clearer value propositions. Online shoppers thus are not immune to the new price environment. As platforms seek higher fees to optimize revenue, sellers must cover these costs, but buyers still expect online shopping to be cheap. Three expectations are currently in tension: higher seller fees, consumer price sensitivity, and brands’ ability to sustain profitability. The result could be ongoing market polarization: established brands with authentic products, strong supply chains, and larger operating budgets may absorb higher costs better; smaller, low-cost competitors face greater pressure. When cheaper players retreat, the risk is a reduced variety of affordable options for price-sensitive consumers. The era of “money is cheap” in e-commerce may be ending. E-commerce remains attractive for Vietnam’s consumers—especially for fast-moving consumer goods and fashion—but the underlying economics are shifting. Online shopping will continue to grow, but not for free. Buyers will still find sales daily, but they must be more discerning about what constitutes real value. Sellers can still reach millions of customers, but at higher costs to achieve visibility. Platforms, having burned cash to shape consumer habits, are seeking to recapture more of those costs. Whether the era of cheap online shopping is truly over remains unclear. There will still be cheap items, deep discounts, and large campaigns, but the days when simply opening an app guaranteed the lowest price are fading.