•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

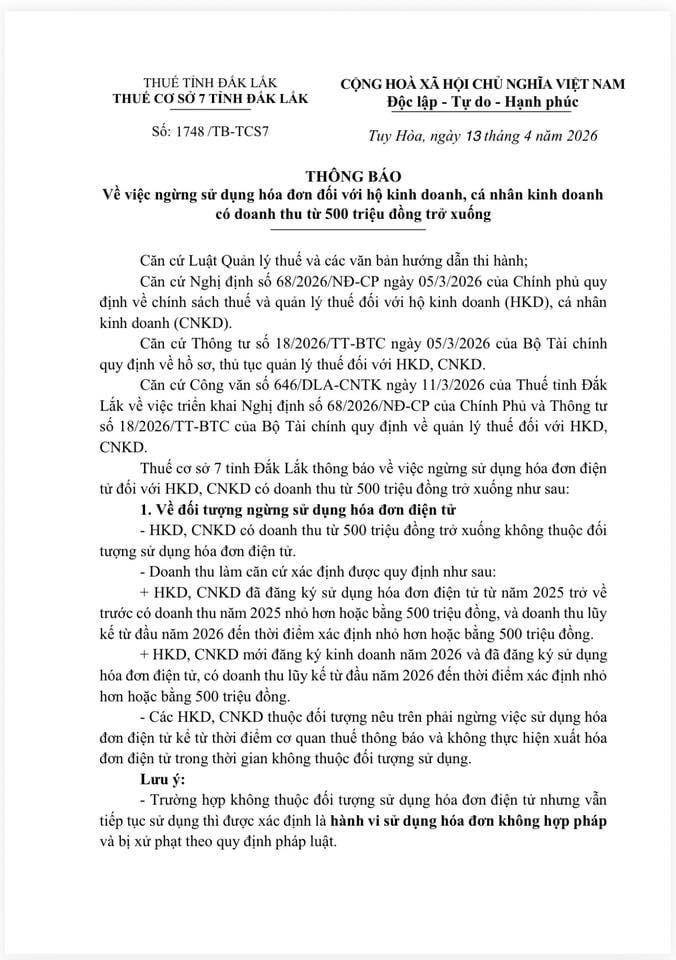

Tax experts say there is currently no basis to sanction micro-business households with annual revenue of up to 500 million VND for issuing electronic invoices. They also call on tax authorities to provide consistent and more flexible guidance for micro-businesses and individuals.

In recent notices, tax authorities in several localities, including Dak Lak and Quang Ngai, instructed micro-businesses and individuals with annual revenue of up to 500 million VND to stop using invoices.

Tax authorities stated that if a taxpayer is not required to use electronic invoicing but continues to issue electronic invoices, it will be treated as illegal invoicing and may be subject to penalties under current law.

After stopping invoicing, micro-businesses and individuals are advised to record revenue in the S1a revenue book, which serves as the basis for tax declarations.

At an online forum on April 14, Nguyen Thi Cuc, chair of the Vietnam Tax Advisory Association (VTCA), said tax authorities have internalized the principle of “no penalties” when enforcement faces issues. She argued that compliant micro-businesses that issue invoices even when not mandatory should not be penalized.

However, she noted that in practice, interpretations and application by local tax authorities remain inconsistent. Some localities consider issuing invoices when not required as a violation that could be penalized, while others provide more flexible guidance, allowing taxpayers to seek assistance in similar cases.

To address the inconsistency, VTCA proposed that the Ministry of Finance and tax authorities issue clear, uniform guidelines. The proposal suggests that micro and individual businesses with annual revenue of up to 500 million VND per year are not subject to VAT and Personal Income Tax, and can still request invoices from tax authorities when customers need them.

VTCA also called for uniform implementation across the tax system to avoid confusion for taxpayers.

Le Van Tuan, director of Keytas Accounting and Tax Co., said that at the end of 2025 and early 2026, tax authorities encouraged micro and individual businesses to use electronic invoices. Many businesses incurred costs for electronic invoicing, digital signatures, or sales software.

He argued that abruptly requiring micro-businesses to stop using electronic invoices would create significant difficulties. He said that if there are reasonable reasons—such as an overloaded electronic invoicing system—the Ministry of Finance or tax departments should explain and guide micro- and small-businesses accordingly.

Under current regulations, electronic invoicing is encouraged for revenues under 1 billion VND. For revenues under 500 million VND, a listing (bảng kê) is used to calculate deductible expenses.

Le Van Tuan questioned why electronic invoicing cannot be allowed instead of requiring a listing. He said the listing increases overall social costs due to paperwork, printing, data entry, and storage, and that explaining to sellers to obtain ID cards is not easy.

He proposed allowing micro-businesses to choose to use electronic invoicing regardless of the revenue threshold.

Further discussions and related updates are continuing as authorities review how the guidance is implemented across the system.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…