•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

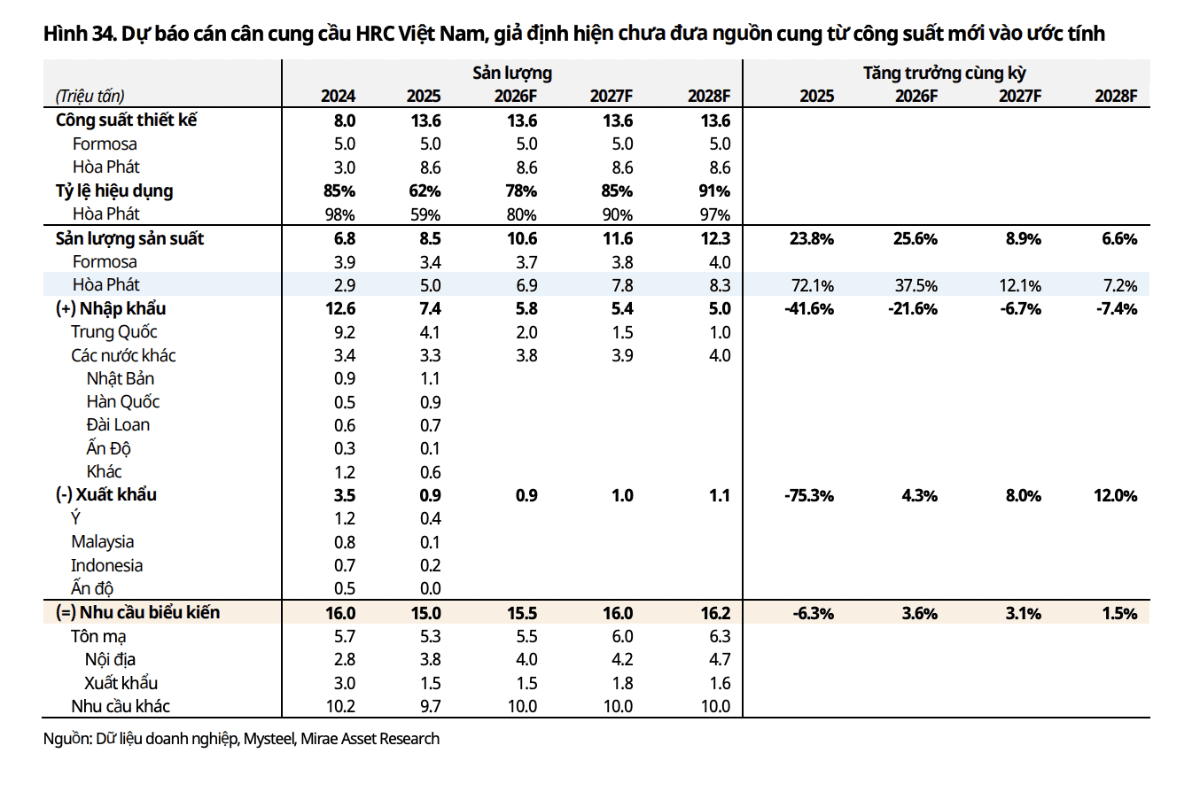

Long-term oversupply risk is a factor to monitor, particularly as many new steel projects are being developed domestically while export prospects remain subdued. Mirae Asset Securities, in an updated outlook for the steel sector, said HRC prices, construction steel, and galvanized steel have started to recover more clearly since the end of Q1 2025.

At the current stage, input costs are playing a more important role than demand in shaping near-term price levels. Rising raw material costs, together with sharp price adjustments in April, suggest steel prices are likely to hold around current levels in the near term as the market waits for further signals from consumption volumes to confirm the trend.

Mirae Asset noted that selling prices for HRC are rising faster than input costs, giving integrated players more flexibility to balance volume growth with selling prices. For galvanized steel, selling prices are expected to stay around 20,000–22,000 VND/kg this year.

In the first six months of 2026, profit margins are expected to be maintained, supported by inventory cycle effects and a widening spread between selling prices and input costs as the gap begins to expand again. The brokerage cited that recent price increases have outpaced the rise in iron ore and coke coal, while inventories purchased at lower prices in Q4 2025 continue to support margins.

Export contributions are expected to remain limited. Although the HRC price gap between ASEAN and the US has been wide in recent years, Mirae Asset said the opportunity to push exports through this differential for Vietnam is almost non-existent. The 25% Section 232 steel import duty nearly eliminates the price advantage, while AD/CVD actions continue to complicate the trade environment.

As a result, the US market remains almost closed to Vietnamese steel despite the rapid rise in steel prices.

In the EU, quota tightening, higher tariffs outside the quota, the CBAM, and stricter origin rules are expected to push HRC prices higher in the medium term. However, these measures are also expected to limit Vietnam’s export growth potential, with export quotas reduced to about half of 2025.

Mirae Asset said HPG is the beneficiary of this trend. The commissioning of Dung Quat 2 boosted HPG’s HRC output to 5 million tonnes in 2025. For 2026, with projected capacity utilization rising from 59% to about 73%, HPG’s output is expected to reach about 6.3 million tonnes, implying a 25% year-on-year increase.

With expectations that HRC demand will plateau or ease slightly, Mirae Asset expects most of HPG’s growth going forward to come from gaining further market share from imports.

On the investment outlook, Mirae Asset said valuations in the steel sector have become more dispersed across groups, reflecting differences in competitive positions and the ability to sustain profits rather than being driven purely by the cycle. Steel prices fell in Q4 2025 and rose again in Q1 2026, and as prices rebound from a trough, the potential for margin expansion is expected to be uneven—continuing the divergence seen previously.

Mirae Asset selected HPG as the stock meeting all criteria for a growth profile, citing volume growth and margin expansion. It is also described as the main beneficiary of structural factors such as anti-dumping duties and the public investment cycle. Accordingly, projected profits are expected to continue rising strongly in the medium term and support valuation over time.

For the target price, Mirae Asset said it continues to benchmark against Indian peers based on similarities in anti-dumping policies and domestic demand growth potential. However, it noted that Vietnam’s steel selling prices over the past year have risen less than in that region.

Even in a less favorable pricing environment, Mirae Asset said HPG has maintained operating efficiency, with operating margins and ROE comparable to Indian steel firms, despite trading at a higher discount.

Nevertheless, long-term oversupply risk remains to be watched, especially as new steel projects are developed domestically while export prospects remain weak. Mirae Asset said HPG is ahead of new projects by at least 3–4 years in investment progress and 10–20 years in operating experience, which it believes gives the company more latitude to consolidate market share, optimize costs, and maintain competitiveness before new supply enters service.

For galvanized steel, Mirae Asset remained cautious as domestic competition intensifies. It said firms must balance production, selling prices, and margins amid rising input costs.

Mirae Asset recommended watching companies where much of the risk has been reflected in valuations. It highlighted GDA, noting a wide gap between its valuation and the 2025 earnings base, alongside modest 2026 growth projections. In 2025, GDA held the second-largest domestic galvanized steel market share at 17%, behind HSG at 22%.

Bitcoin (BTC) investors who use steady dollar-cost averaging (DCA) may be underperforming versus strategies that adjust exposure to the market’s cycle, according to new research arguing that Bitcoin’s behavior differs from traditional long-duration assets.

In a report cited by Markus Thielen of 10x Research, Bitcoin’s market…