•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

The reverse winds from interest rates, geopolitics and oil prices are gradually easing, leaving the market with an unusually low valuation floor. In this context, capital is quietly returning, creating accumulation opportunities for patient investors.

The stock market has stabilised and advanced for several consecutive sessions, suggesting that demand remains receptive. Analysts interpret this as a sign that a short-term bottom may be forming, with “grounds to believe” that the VN-Index has formed a bottom.

The rebound is attributed to the convergence of several factors. The market has welcomed confirmation of an upgrade path, leadership changes, and expectations that monetary policy will ease. In addition, easing geopolitical tensions and a sharp drop in oil prices have improved investor sentiment.

Mirae Asset (MASVN) pointed to a historical similarity in 2025. When President Trump announced delaying hardline tariff and military statements to allow for negotiation, the 10-year U.S. Treasury yield rose above 4.3%.

On March 23, Trump announced postponement of air strikes on Iran’s energy infrastructure. Prior to that announcement, the 10-year yield had reached its highest level since July 2025.

MASVN said markets typically form a bottom when uncertainty is at maximum and there is a signal of a shift from escalation to negotiation. It noted that market reactions to the March 23 announcement resemble the bottoming moment in mid-April 2025, when Trump announced a 90-day delay to negotiate counter-tariffs.

“There are grounds to believe the market may have formed a bottom even though it subsequently continued to be volatile due to subsequent statements/news,” MASVN concludes.

MASVN cited a potential basis for cooling in the next 4–5 weeks, including the approach of the US midterm elections in November and US labor market data showing a cooling trend.

The aim is to avoid a “stagflation trap” by cooling the war to prevent persistent inflationary pressure that could force the Fed to delay rate cuts.

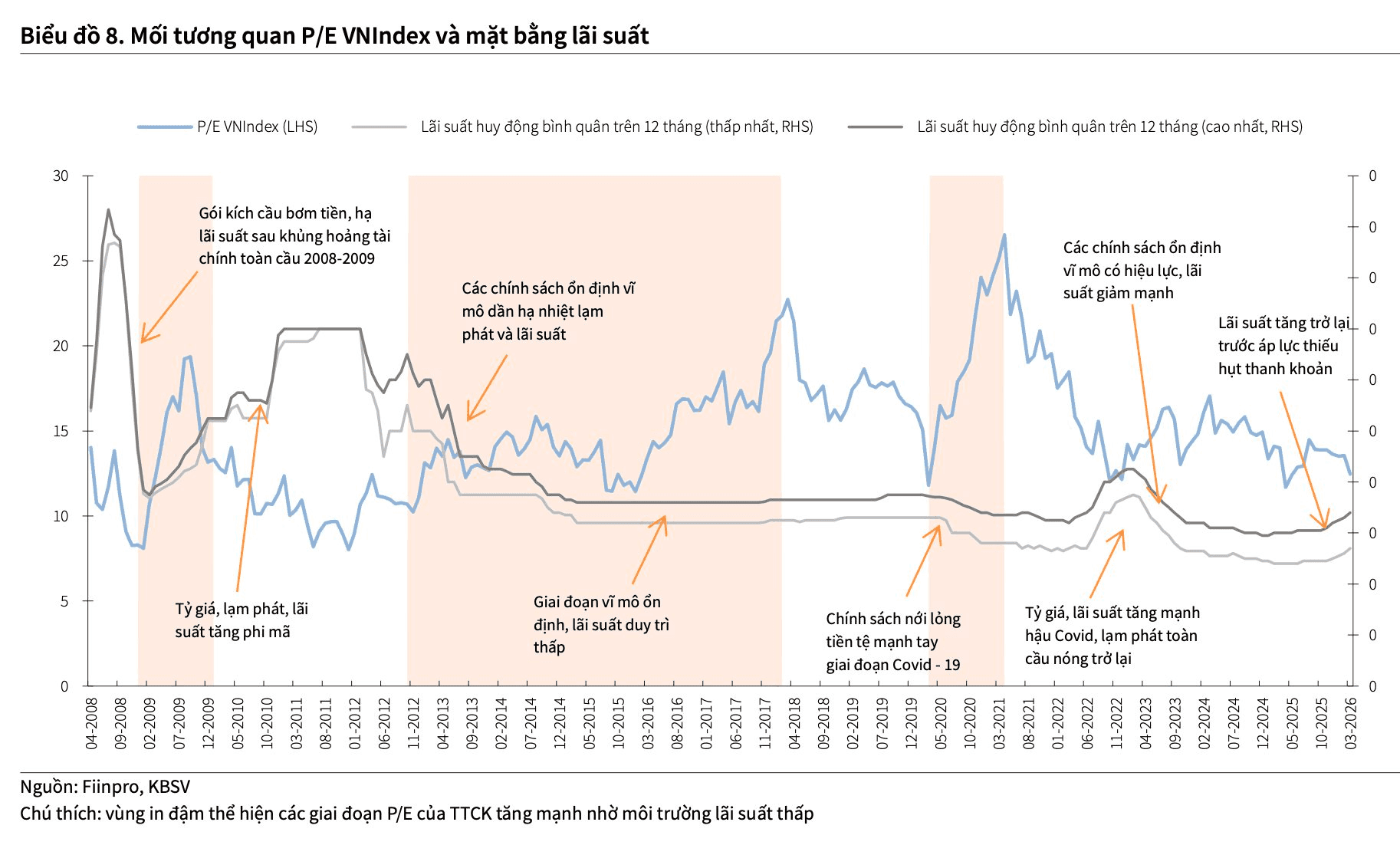

Valuation remains attractive. In addition to recovery signals and bottom-formation potential, valuation metrics such as P/E and P/B are below the 10-year average. Earnings prospects (ROE) are also described as entering an improving cycle due to structural economic changes and positive sector shifts.

MASVN added that if a few large-cap stocks with sharp gains and dominant index weight are excluded, overall market valuations become even more attractive.

On March 23, the VN-Index recovered after the P/E ratio touched the long-run average minus one standard deviation (about 14.4x). MASVN forecast that momentum could continue, noting that the P/E is currently around 16x, still attractive versus the long-run average of 17x.

Historical data cited by MASVN shows a similar market structure in April 2025. After the countervailing tax was announced on April 2, 2025, a one-week crash (April 2–8, 2025) pushed the P/E from 14.8x to 12.3x, before recovering strongly to 17.3x.

Phung Minh Hoang, Head of Strategy at Phu Hung Fund Management, said detrimental factors such as high interest rates, geopolitical tensions, and oil price volatility have been reflected in stock prices, leaving the market trading at relatively low valuations. He suggested that Q2 2026 could be an appropriate time to begin participating, particularly with a long-term approach.

In a more positive scenario, Hoang expects macro indicators to improve in the latter half of 2026 as interest rates ease and geopolitical tensions gradually fade, meaning current headwinds are viewed as short-term.

Luong Duy Phuoc, Director of Analytics at KAFI Securities, said that if a bottom forms successfully, leading stocks are likely to be those sensitive to looser financial conditions—such as banks, securities, and real estate—because these sectors typically react quickly when pressure on interest rates, exchange rates, and risk sentiment eases.

He added that money could then flow to stocks that were heavily sold during the correction but whose business foundations are not significantly affected by oil prices or geopolitical factors, including some retailers, technology, industrial parks, and construction materials. The experts said that if the recovery becomes more sustainable, opportunities may appear across both financially sensitive groups and stocks that are deeply discounted relative to intrinsic value.

Voong Khac Huy, Head of Analytics and Investments at Dai-ichi Life Vietnam, stressed that investors should focus on the broader economic picture rather than short-term fluctuations. He said that in a context of positive growth, opportunities will not be evenly distributed, and the “investment compass” in the next phase will take a “K” shape—meaning capital concentrates in a limited set of firms rather than spreading widely.

Overall, the article highlights potential bottom formation and the importance of selective, long-term investing as the market transitions toward more favorable macro and sector dynamics.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…