•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

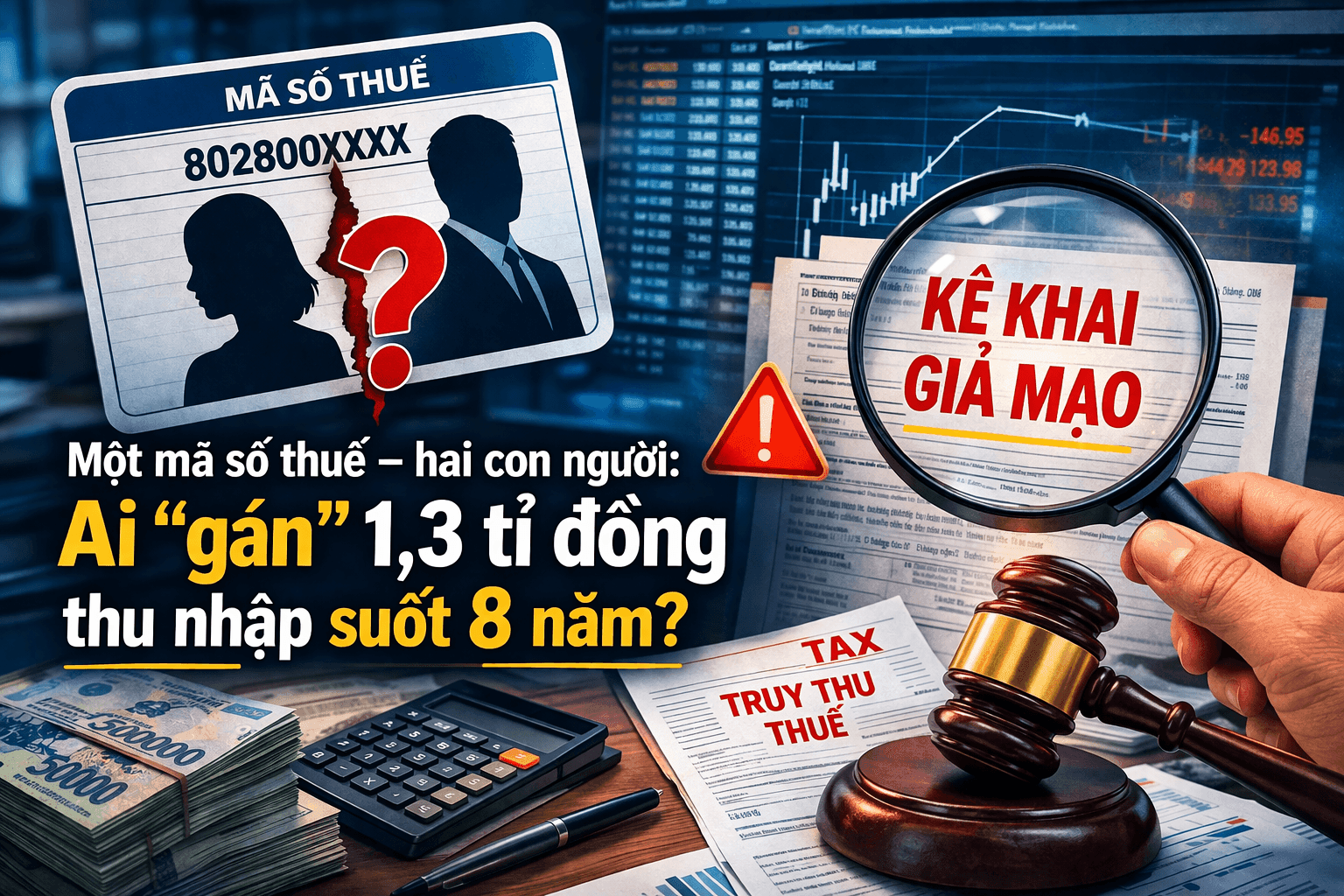

An individual who said she had never worked was unexpectedly recorded as having earned more than 1.3 billion VND over several years, and she is now facing back personal income tax of about 93.6 million VND. Ms. O., born in 1970 and residing in Bình Quới Ward, Ho Chi Minh City, has worked at the Ho Chi Minh City College of Agricultural Engineering since 2008 and authorized the agency to finalize her annual personal income tax.

In early 2026, while reviewing her tax settlement data, Ms. O. found that the college attributed income to her tax profile for the period 2017–2024, totaling over 1.3 billion VND. Based on that record, the personal income tax payable was calculated at 93.6 million VND. Ms. O. said she never worked at the institution, did not sign a contract, and did not receive any income from the college.

The case highlights the risk that, if such “income dropped from the sky” is not detected, the taxpayer could be treated as a high-income earner, potentially triggering additional tax obligations and raising questions about whether declarations were properly made. The college denied ever employing Ms. O. and said it is cooperating with the tax authority to verify the use of her tax code.

However, tax data show the institution recorded her as an employee from 2015 to 2024. Even after Ms. O. received a denial letter from the school on January 27, 2026, the income attribution remained in the tax system.

A first-level audit reportedly found that from 2016 to 2024, the Ho Chi Minh City College of Agricultural Engineering reported income payments to an individual identified as L.T.B.T. The tax code used for L.T.B.T was stated to match Ms. M.T.P.O.’s tax code, but it did not match the national data for the purported recipient.

In effect, the same tax code was assigned to two different individuals, which the article describes as a sign of serious data governance problems.

According to Lương Thế Phúc, Vice Rector in charge at the college, L.T.B.T is a teacher at the school. The institution said it would follow the law and report to the competent authority if the issue is beyond its authority.

The central question raised is how such a significant discrepancy could persist for nearly a decade without being detected.

Attorney Trần Văn Tuấn said the situation shows signs of violations in tax management and the use of personal data. Under the 2019 Tax Management Law, employers must declare income truthfully and accurately, and taxpayers have the right to request adjustments when errors are found.

He noted that using someone else’s tax code to declare income cannot be treated as a routine technical mistake. If there is evidence of deliberate actions to formalize payments or evade tax obligations, those involved could face administrative penalties and, depending on the elements of a crime, potential criminal liability.

The article also points to privacy and data protection concerns arising from income being misattributed for nearly eight years. It further argues that the discrepancy across multiple settlements suggests a flaw in the data reconciliation mechanism—particularly if the system fails to detect errors and the burden shifts to individuals to protest.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…