•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

VN-Index fluctuated sharply as it tested the January 2026 high zone of around 1,900–1,920 points. Technical indicators showed weakening momentum: the Stochastic Oscillator continued to decline and the MACD gap toward the signal line narrowed. If the MACD crosses below the signal line in upcoming sessions, short-term risk is expected to rise.

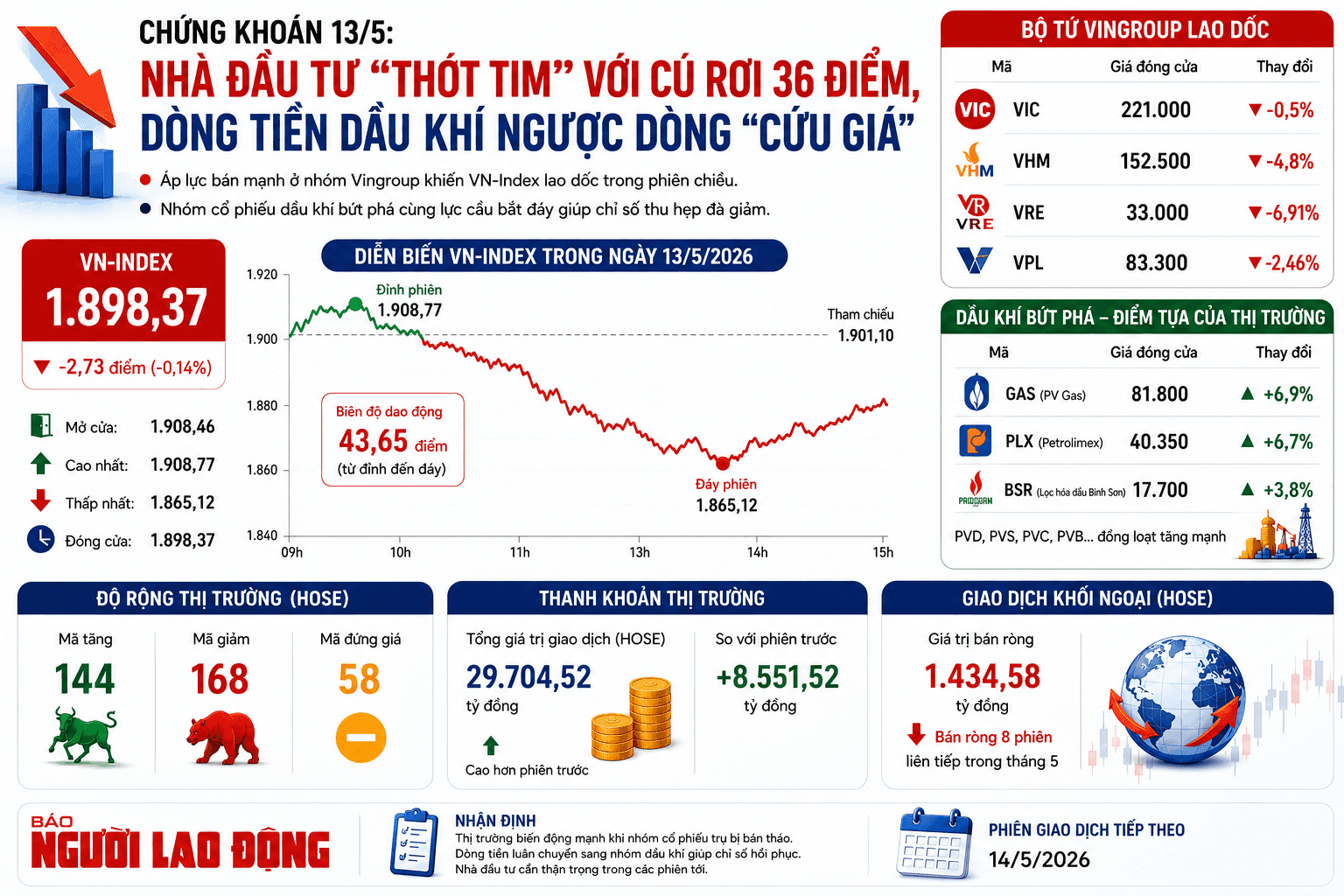

On May 13, 2026, major indices moved in mixed directions. The VN-Index fell 0.14% to 1,898.37 points, while the HNX-Index rose 0.53% to 254.62 points.

Trading activity increased. On HOSE, turnover rose 23.3% to nearly 797 million shares. On HNX, more than 62 million shares changed hands, up 47.3% from the previous session.

Foreign investors remained net sellers, with estimated net selling of about 1.5 trillion VND on HOSE and more than 60 billion VND on HNX.

Downward pressure appeared early in the session as large-cap leaders weakened, pushing VN-Index below the previous close for most of the morning. In the afternoon, volatility intensified as the index swung; Vingroup-related components weighed briefly toward around 1,865 points. However, selling did not broaden into panic, and buying demand returned, allowing the index to close with only a modest decline.

At the close, VN-Index finished at 1,898.37 points, down 0.14% from the prior session. Market performance also showed dispersion, with VS-LargeCap, VS-MidCap, and VS-SmallCap ending near the flat line amid alternating gains and losses.

Several stocks contributed to the index’s decline. VHM was the largest drag, subtracting 6.43 points. VIC, STB, and VRE also reduced the index by a combined total of about 4 points. Meanwhile, Gas, BID, BSR, and MCH helped cushion losses.

The VN30-Index fell 10.46 points (-0.51%) to 2,043.51. Market breadth showed 15 decliners, 13 risers, and 2 unchanged. On the upside, GAS led gains, followed by PLX, BSR, and BID (each up more than 2%). On the downside, VRE saw profit-taking, alongside VHM and STB (down 4.8% and 4.3%, respectively).

By sector, energy continued to lead, rising 4.27%, supported by BSR (+3.78%), PLX (+6.75%), PVS (+2.5%), PVD (+6.44%), PVT (+4.42%), and PVP (+6.59%). Utilities and media-related services also traded positively, including GAS at the ceiling price, POW (+1.07%), VGI (+7.21%), FOX (+1.93%), CTR (+4.12%), YEG (+1.52%), and VTK (+3.07%).

Real estate lagged. VRE hit the lower circuit, while major real estate names such as VHM, KSF, KBC, KDH, TAL, IDC, NLG, and DXG all declined.

VN-Index: MACD narrowed against the signal line as the index tested the January peak around 1,900–1,920. The Stochastic Oscillator remained weak. A cross below the signal line would increase near-term risk.

HNX-Index: HNX extended its advance for the third session and stayed above the middle Bollinger Band. MACD has crossed above the signal line; if it continues rising and clears 0, the near-term recovery would be strengthened.

Money flow: The Negative Volume Index for VN-Index remains above the 20-day EMA. If this holds, downside thrust risk is assessed as limited.

Foreign flows: Foreign selling persisted on 13/05/2026. Continued net selling in upcoming sessions could increase downside pressure.

Market statistics and regional index visuals were included in the original report, prepared by Vietstock Economic & Market Strategy Department and Vietstock Advisory.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…