•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Brokerages issued positive outlooks for DCM, HDB and SAB, recommending “Buy” across the three stocks. The notes cited supportive industry pricing, improving earnings momentum, and specific catalysts tied to each company’s operations and capital-market activity.

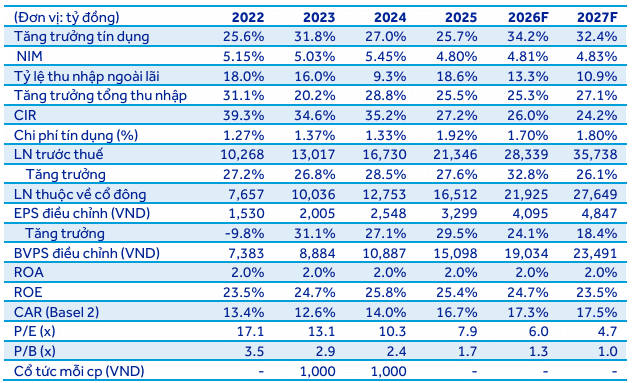

ACBS raised its 1-year target price for Ho Chi Minh City Development Joint Stock Bank (HDB) by 13.4% to 30,000 dong per share and maintained a positive view, citing a 2026 earnings upgrade of 12.3%.

The target price is based on a 7.0x forward price-to-earnings ratio, aligned with the historical median. ACBS expects HDB’s 2026 pretax profit to continue growing strongly, forecasting 28,187 billion dong, up 33% year-on-year and slightly above the company’s approved plan.

High credit growth is highlighted as the main driver of profit growth in 2026. As part of the responsibility for reorganizing VikkiBank, the State Bank of Vietnam granted HDB a credit-growth limit of up to 35%. This compares with the SBV’s broader target of roughly 15% credit growth in 2026, down from 19% last year. Other banks not taking on the same restructuring risk are limited to 11–12% growth.

Net interest margin (NIM) is forecast to be flat at around 4.8%, supported by rising lending rates, though offset by higher funding costs. The brokerages also noted that HDB’s liquidity remains solid, helping limit cost-of-capital pressure in a stressed banking environment.

Asset quality could face pressure in 2026. A high-rate environment may strain borrowers in real estate and construction—sectors that account for roughly 34% of HDB’s loan book. ACBS projects the non-performing loan (NPL) ratio to rise to 2.5% in 2026 from 2.1% in 2025. Provisions are expected to increase by 15.2%, citing a high base of loan-loss reserves in the prior year. The bad-loan coverage ratio is expected to remain around 52%.

Overall, HDB’s 2026 earnings are still expected to grow robustly, but higher interest rates could weigh on asset quality across the banking sector, where HDB is considered particularly sensitive due to its exposure to consumer lending and real estate.

ACBS pointed to several catalysts for HDB’s share price, including bond-to-equity conversions, private placements with foreign strategic investors, and an IPO and listing of HDBS (HDB owns 30%) in the second half of 2026. Additional potential catalyst mentioned is the possible conversion of its subsidiary HD Saison into a joint-stock company.

FPTS recommended tracking SAB at 43,400 dong per share, with a target price of 49,900 dong per share, implying about 15% potential upside from the entry price.

FPTS projects SAB 2026 revenue of 26,364 billion dong and net profit after tax of 4,763 billion dong, up 1.8% and 4.1% respectively versus 2025. For 2027–2030, revenue and net profit are projected to grow by 43% and 2.8% per year.

SAB’s near-term outlook is described as neutral, with slight margin expansion driven by lower malt prices and a favorable high-rate environment. Beer volume is expected to recover about 1.8% from a weak 2025 base as retailers adapt to new tax regulations. However, the recovery may remain modest due to consumer spending pressures from rising inflation.

For 2026, the net profit margin is projected to improve by 0.4 percentage points, supported by a 0.2 percentage point rise in gross margin as malt prices trend lower and aluminum prices are offset. Financial income is forecast to rise by 18.4%.

In the longer term, SAB’s growth is expected to be modest due to intense competition. Beer volume is forecast to grow at about 4.3% per year on a recovering industry backdrop, but this is about 0.7 percentage points lower than the broader sector, attributed to aggressive competition and marketing spend controls.

Net profit margin in 2026 is expected to improve as aluminum price dynamics and the high-rate environment influence margins, while higher financing income supports earnings growth.

Risks mentioned include a prolonged US–Iran conflict that could push aluminum prices higher.

Brokerages recommended “Buy” for Ca Mau Fertilizer Joint Stock Company (DCM) with a target price of 54,900 dong per share. KB Vietnam (KBSV) noted that Q4 2025 revenue and net income were 4,302 billion dong and 434 billion dong, down 1.9% and 16.7% year-on-year, respectively, while full-year 2025 results showed 24% revenue growth and 38% net income growth.

KBSV expects tight supply-demand dynamics to keep urea prices high, supported by global supply disruptions from the Hormuz Strait and China’s export controls. Demand from large markets such as India is also expected to remain strong ahead of peak season, providing price support into H2 2026.

KBSV projects DCM’s earnings growth to be driven by margin expansion, supported by the favorable spread between high urea prices and slower input gas costs. The broker also cited the new VAT policy as improving competitiveness and cost efficiency, providing a driver for medium-term growth from both market and policy factors.

With DCM stock up roughly 30% year-to-date, KBSV views DCM as an attractive mid-term investment. Using FCFF and EV/EBITDA valuation methods, KBSV supports a Buy rating with a target price of 54,900 dong per share, representing 16.8% upside to the close on 13/04/2026.

Further details were referenced in the linked reports from ACBS, FPTS and KBSV.

Bitcoin (BTC) investors who use steady dollar-cost averaging (DCA) may be underperforming versus strategies that adjust exposure to the market’s cycle, according to new research arguing that Bitcoin’s behavior differs from traditional long-duration assets.

In a report cited by Markus Thielen of 10x Research, Bitcoin’s market…