•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

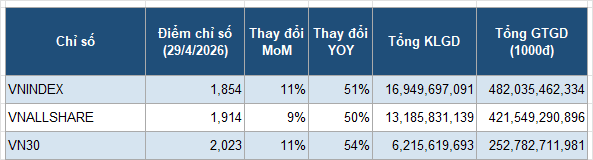

As of the close of trading on April 30, 2026, the VN-Index stood at 1,854.1 points, the VNAllshare at 1,913.7 points, and the VN30 at 2,022.75 points. In April, all three main indices recorded positive monthly gains, rising 10.73%, 9.46%, and 10.56%, respectively, compared with the previous month.

By the end of April 2026, the market’s three key benchmarks all ended higher, reflecting broad-based strength across large-cap and overall market segments.

Sector performance in April showed clear divergence. The real estate group (VNREAL) rose sharply by 43.2%, while financials (VNFIN) and construction materials (VNMAT) increased by 3% and 2.1%, respectively.

In contrast, several sectors declined, including energy (VNENE) down 9.3%, healthcare (VNHEAL) down 8.9%, and utilities (VNUTI) down 4.13%.

Liquidity in April 2026 followed a cooling trend. For equities, the average daily trading volume exceeded 847.48 million shares, with average daily trading value of about 24,101 billion VND. Compared with March, this represented a decline of 19.6% in volume and 20.7% in value.

The market for assured warrants (CW) decreased modestly. Average daily trading volume was above 62.63 million units, and daily value reached 83.29 billion VND, down 5.92% in volume and 1.35% in value versus March.

ETF certificates saw a sharper contraction. Average daily volume was 1.79 million units and daily value was 60.73 billion VND, down over 55% compared with March 2026.

As of the end of April 2026, HOSE had 690 listed and traded securities, including 402 stocks, 4 closed-end funds, 18 ETF funds, and 266 CWs. Total listed volume surpassed 215.39 billion shares.

Stock market capitalization totaled about 8,726 trillion VND, up 10.82% from the previous month. This figure is equivalent to 67.92% of 2025 GDP and accounts for more than 95% of total market capitalization.

As of the end of April, 54 companies had market capitalizations above USD 1 billion. Five companies surpassed USD 10 billion: Vingroup (VIC), Vinhomes (VHM), Vietcombank (VCB), BIDV (BID), and VietinBank (CTG).

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…