•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

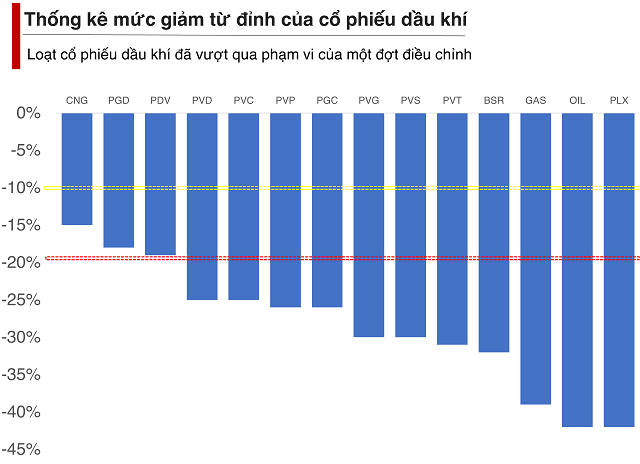

After a hot rally in early 2026, the oil and gas stock group is entering a deep pullback as many names have discounted 30%–40% from their peaks, just ahead of the Q1 2026 earnings results season. The move is prompting questions about how much upside remains for a cyclical sector.

Following historical highs, several oil and gas shares have recorded steep declines from peak levels. BSR and PVS have discounted by more than 30% from their all-time highs, while OIL and PLX have fallen as much as 42% and GAS has lost around 39%.

As of the close of trading on Apr 10, investors who bought near peak levels are now facing large losses, with the stocks largely in bear market territory.

Despite the recent sell-off, the broader picture is not uniformly negative. Since the start of 2026, many sector stocks have still posted gains even as signs of cooling emerge in the context of the Gulf confrontation.

As of the close of trading on Apr 11, BSR was up 66.1%, PVC up 52.2%, OIL up 40.7%, PVD up 19.6%, PLX up 16.6%, and PVS up 15.5%.

This suggests the group’s decline has extended beyond a typical correction, but it has not fully formed the “Christmas tree” pattern often associated with purely speculative stocks. Money flow, based on the continued gains versus early-2026 levels, has not completely exited the names mentioned.

Recently, Bình Sơn Refinery and Petrochemical Company (BSR) reported Q1 output of over 2.03 million tons, up 13% year-on-year. Revenue reached over 41,278 billion VND, up 28%, averaging more than 450 billion VND per day.

For 2026, BSR targets consolidated revenue of over 154,140 billion VND and after-tax profit of 2,162 billion VND. This implies revenue up 25% and after-tax profit down 58% versus 2025 actual results, according to the information referenced in the article.

MBS Securities said oil and gas company revenues could grow positively due to high fuel prices while supply is not expected to be significantly constrained. MBS also expects crack spreads to recover strongly in Q1 2026, which would support margins for refining and petrochemical companies such as BSR.

MBS further expects 2026 net profit to rise sharply versus the low base of the prior year, mainly due to improved crack spreads.

In the near term, oil prices are expected to remain high and volatile amid geopolitical developments, which could support revenue and project backlogs. MBS noted that upstream would benefit most if oil stays above break-even, boosting exploration and production (E&P) activity and increasing demand for oilfield services; this segment is also described as the most sensitive to oil price fluctuations.

Midstream is expected to benefit more steadily from mid- to long-term contracts, with less volatile revenue and cash flow, though with limited growth potential. Downstream is expected to gain from higher crack spreads and rising retail prices, but it may face input cost pressure and supply risks if oil remains high for an extended period.

From a cautious perspective, Mr. Bùi Văn Huy, Director of Investment Research at FTID, said the oil and gas group depends heavily on oil prices, but financial results often lag and may take several quarters to fully reflect oil-price changes.

He also highlighted that many sector companies have significant government ownership, which can affect operating efficiency, while broader economic support is needed to help translate oil-price advantages into actual profits.

Macro pressure is another key risk. Mr. Huy said oil prices would need to drop to around 85 USD per barrel to reduce inflation and exchange-rate pressures. If oil prices remain high, macro risks could rise and weigh on financial markets in general and oil stocks in particular.

Bitcoin (BTC) investors who use steady dollar-cost averaging (DCA) may be underperforming versus strategies that adjust exposure to the market’s cycle, according to new research arguing that Bitcoin’s behavior differs from traditional long-duration assets.

In a report cited by Markus Thielen of 10x Research, Bitcoin’s market…