•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

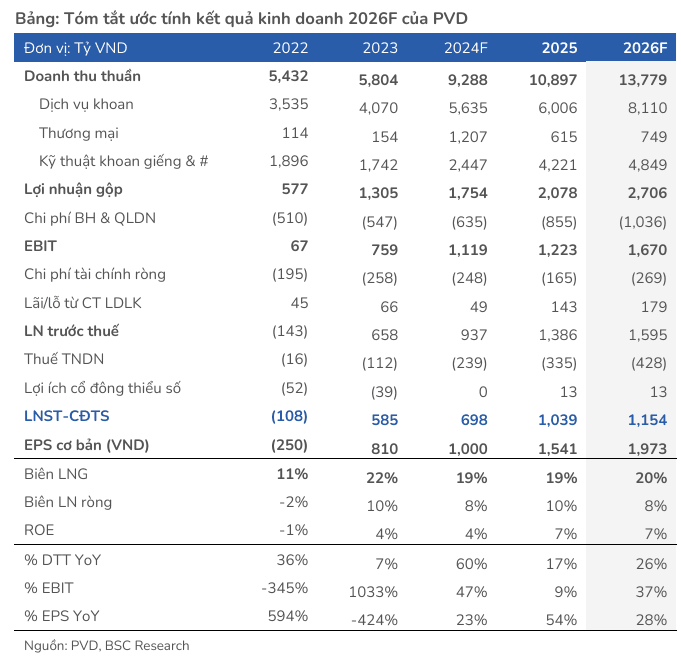

Brokerages recommend Buy for PVD due to growth prospects supported by higher jack-up rig lease rates and contributions from new rigs; GAS is rated Neutral as margins come under pressure even though results continue to grow on higher gas prices; and TNG is rated Buy on expectations of orders recovery and higher profit growth as the textile sector stabilizes. Buy PVD with a target price of 39,450 VND per share. PVD has Buy ratings from BIDV and BSC, with a target price of 39,450 VND, based on a 50/50 weighting of EV/EBITDA and DCF. They forecast 2026 net revenue of 13,779 billion VND, up 26% year-on-year, and net profit of 1,154 billion VND, up 11% (up 28% if 2025 non-recurring income is excluded), implying an EPS of 1,973 VND; forward P/E around 16.9x and EV/EBITDA about 7.8x. This outlook rests on assumptions of a 6% improvement in rig lease rates and contributions from new PVD VIII and IX; drilling services segment is expected to grow 15% from a high base in 2025. Q1 2026 results are projected: net revenue of 3,500 billion VND, doubling year-ago levels, and pre-tax profit of 400 billion VND, up 100%. For 2025, net revenue was 10,897 billion VND, up 17% and net profit 1,039 billion VND, up 49%, beating BSC’s forecast by 24%. At the 2026 AGM, the company approved a 66.9% capital increase to 9,282 billion VND to widen borrowing and bidding capacity; cash dividends were suspended to prioritize rig investment. The 2026 net profit target is conservatively set at 800 billion VND (−22.8% y/y). In drilling-well services, demand from the Lô B – Ô Môn project (estimated 40–50 wells/year) provides a stable workload; 2026–2027 revenue is forecast at 4,000–5,000 billion VND/year, up 153% with gross profit around 1,000 billion VND/year, up 188% versus the 2022–2024 base. Contributions from PVD VIII and IX in drilling services are expected; Jack-up drilling revenue is projected to rise 41% in 2026 due to more rigs and higher spot hire rates, with Q1 2026 spot rates at a new peak around 99,200 USD/day, up 33% versus 2025 average. Risks for PVD include crude oil price volatility affecting lease rates upon contract renewals; high debt service costs and unhedged FX losses when revaluing foreign debt; delays in revenue ramp from new rigs and bottlenecks on the Lô B mega-project affecting backlog. GAS: MBS projects Q1 2026 net profit of 3,307 billion VND, up nearly 20% YoY; 2026 and 2027 net profits are forecast at 13,227 billion and 14,896 billion VND, up 15.9% and 12.6% respectively as LNG enables growth. MBS revises 2026 gross margin down by 5.1 percentage points from prior estimates; 2026 net profit at 13,227 billion (up 15.9%), 2027 at 14,896 billion (up 12.6%). The target price is 83,800 VND, modestly down 1.3% from prior due to re-pricing, with a Neutral stance reflecting valuation levels. LNG projects domestically are not yet fully reflected in near-term earnings. TNG: Mirae Asset uses a DCF approach to value TNG (HNX) with a 13% required return and 0% long-term growth post-2036; the target remains 26,500 VND, upgraded to Buy from Hold as the stock price has declined. Macro context shows Vietnam’s garment exports holding up, with March and Q1 2026 export values at USD 3.1 billion and USD 8.8 billion respectively; domestic production steady as IIP rises; however, raw-material imports (cotton and fabric) show signs of softening. Energy prices elevated by Middle East tensions raise costs for manufacturers. In Q1 2026, TNG revenue rose 29% to 1,952 billion VND; gross margin fell to 12% (vs 15.2% in Q1 2025) with gross profit of 236 billion VND. Finance income was largely flat while finance costs rose 9.2% due to higher debt; selling expenses grew 46.4% amid higher freight costs. Operating profit declined modestly to 51 billion VND; an abnormal gain of 25 billion VND was recorded in the quarter. Net profit for Q1 2026 was 60.3 billion VND, up 39%. For 2026, Mirae Asset projects operating profit of 601 billion VND (up 26.5%) and net profit of 493 billion VND (up 25.4%), with revenue of 9,300 billion VND and gross margin of 15.4%. Key costs, especially financial costs and SG&A, are expected to rise due to inflation. Overall, the research notes suggest cautious positioning given macro risks and input-cost pressures in the garment sector.

Bitcoin (BTC) investors who use steady dollar-cost averaging (DCA) may be underperforming versus strategies that adjust exposure to the market’s cycle, according to new research arguing that Bitcoin’s behavior differs from traditional long-duration assets.

In a report cited by Markus Thielen of 10x Research, Bitcoin’s market…