As of 12 March 2026, the spread between USD buy and sell rates at commercial banks narrowed sharply compared with the start of the month, falling from 410 dong per USD to 270 dong/USD—down more than 34%. The tighter gap points to lower market risk and more stable sentiment.

On 12 March, the State Bank of Vietnam (SBV) published the central USD/VND rate at 25.061, up 2 dong from 11 March. The SBV’s USD/VND ceiling rate is 26.314, corresponding to a band of +/- 5% around the central rate.

Since the start of March, the SBV has kept the central rate moving within a very narrow range around 25.059–25.062 in response to global fluctuations and Middle East tensions. This has helped commercial banks maintain relatively stable selling rates.

On 12 March, the selling rate at commercial banks was 26.314 VND/USD, up 3 dong from 11 March and close to the SBV ceiling. Compared with early March, the selling rate rose by about 5 dong.

Buying rates at banks moved up and down. After a strong rise on 9 March, buying rates fell on 10 March and then recovered, reaching 26.044 VND/USD on 12 March. This was up 45–50 dong from early March depending on the bank.

With buying at 26.044 and selling at 26.314, the bank spread on 12 March hovered around 270 dong per USD, down from the 410–500 dong range seen earlier in the month.

In the interbank market on the same day, the USD/VND rate traded around 26.273, up 0.05% from the previous day and 0.18% from the prior week, but down 0.08% from the start of the year.

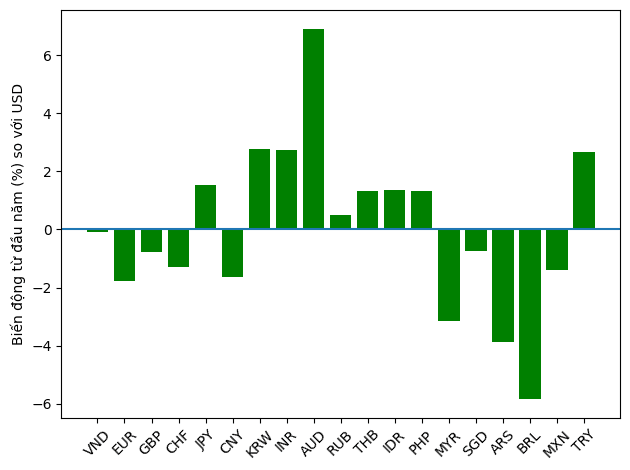

Since the start of 2026, currency moves across Asia against the USD have diverged. The Vietnamese dong (VND) has generally been stable, up about 0.08% versus the USD. Singapore’s SGD is up 0.75%, and China’s CNY is up 1.63%.

By contrast, several regional currencies weakened versus the USD, including Korea’s KRW (down about 2.77%). Thailand’s THB, Indonesia’s IDR, and the Philippines’ PHP were also weaker by about 1.3%.

Overall, the VND remains among the most stable currencies in the region year-to-date, with relatively small volatility against the USD.

On the free market today, the USD price is around 27,150–27,190 VND/USD (buy–sell).

Since early March, the free-market USD/VND rate has risen sharply following the escalation of the Iran–Israel–United States conflict. It increased by about 300 dong on 9 March, then largely held flat or eased slightly.

As of today, the free-market USD price is higher than the bank rate by about 876 dong on the sell side and 1,106 dong on the buy side.

Inflation pressure in the United States has remained elevated, supporting a stronger USD that can affect exchange rates globally. The US CPI for February rose 0.3% month-on-month, while core CPI rose 0.2% after increases of 0.2% and 0.3% in January. On a year-on-year basis, headline CPI rose 2.4%, unchanged from the previous month and in line with expectations.

These data indicate inflationary pressures remain relatively high and could intensify amid Middle East tensions. Oil prices, though off the near-term high near 120 USD per barrel, remain elevated and continue to weigh on the global economy.

Against this backdrop, expectations for Fed monetary policy easing have narrowed. CME-based projections indicate the Fed could cut the policy rate only once in September this year, instead of twice as previously anticipated. Markets are awaiting the Fed meeting on 17–18 March for further signals on the policy outlook.

The U.S. Dollar Index (DXY) at 12:00 on 12 March stood at 99.47, up 0.24% from the previous session and 0.15% from the prior week. Year-to-date, the DXY has risen 1.16%, though it remains about 4.86% below its 52-week high. A stronger dollar can continue to exert pressure on exchange rates in many economies, including Vietnam.