•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

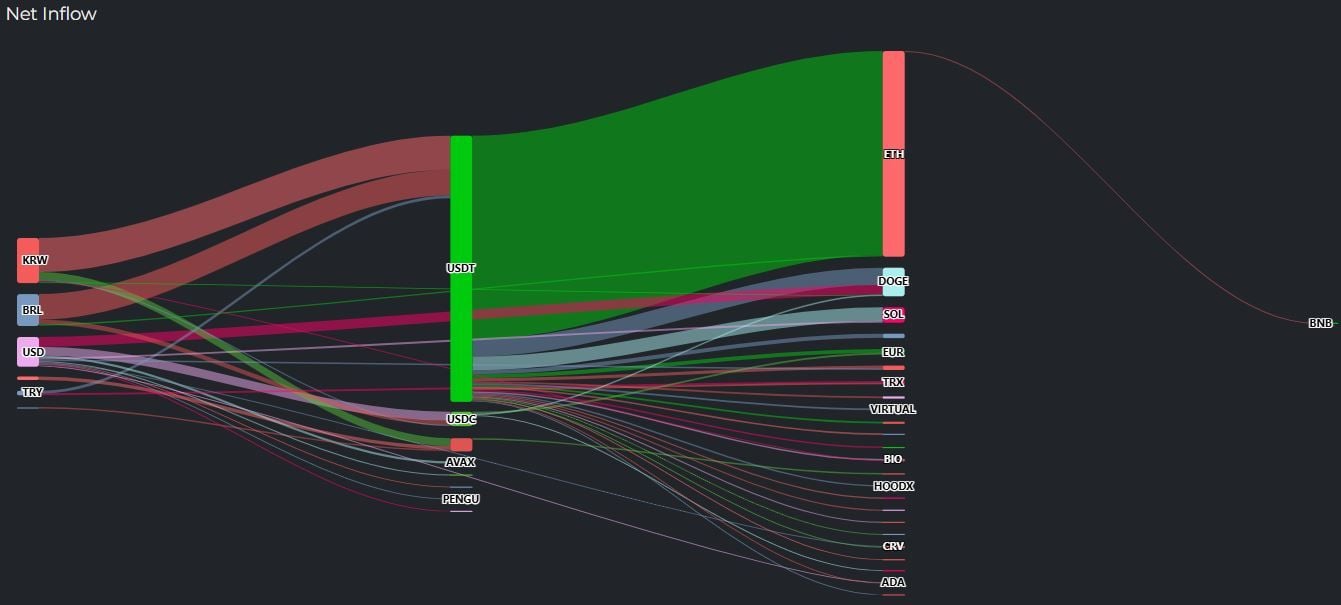

Capital rotation in the crypto market accelerated late Wednesday ET, with nearly $29.85 million worth of Tether (USDT) moving across multiple tokens even as Ethereum (ETH) recorded a notable net outflow. The pattern suggests short-term repositioning rather than a single, clear directional bet.

Data compiled by Cryptometer showed that over the past five hours as of 9:50 a.m. ET on Thursday (10:50 p.m. Wednesday in Korea), fresh fiat-linked inflows into crypto included approximately $5.04 million in South Korean won (KRW), $3.54 million in Brazilian real (BRL), and $3.29 million in U.S. dollars (USD).

Within stablecoins, the more prominent move was the redistribution of about $29.85 million in USDT into a basket of cryptocurrencies.

Despite the USDT-to-ETH rotation, Ethereum (ETH) also recorded the biggest net outflow on the sell side, with roughly $11.38 million leaving the asset over the same five-hour window. Bitcoin (BTC) saw about $9.18 million in outflows.

Smaller but notable selling pressure appeared across additional assets:

Stablecoin positioning also moved. Cryptometer data indicated roughly $7.38 million consolidated back into Tether (USDT), including about $2.47 million that moved into USD. USD Coin (USDC) absorbed inflows totaling around $4.54 million, indicating some traders parked liquidity in alternative stablecoin rails rather than staying fully exposed to market volatility.

In fiat conversions, USD accounted for the bulk of cashing-out flows at roughly $15.39 million, followed by KRW at about $4.68 million and EUR at about $1.26 million.

The combined pattern—USDT dispersing into risk assets while BTC and ETH simultaneously show net outflows—points to two-way flows typical of short-term trading environments, where buyers and sellers actively reshuffle exposure instead of committing to a unified trend.

Going forward, sustained stablecoin redeployment into majors like Bitcoin (BTC) and Ethereum (ETH), paired with declining fiat conversion, would typically suggest improving risk appetite. For now, the data reflects a market balancing opportunistic dip buying with profit-taking and de-risking.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…