•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Market divergence is drawing attention as major indexes reach fresh highs while underlying breadth remains narrow and liquidity stays weak. Investors are watching the gap between index performance and market participation, with some warning that if breadth and liquidity do not improve soon, the risk of a technical correction near the peak could rise.

The S&P 500 rose above 7,400 for the first time. Major Asian markets, including Korea, Japan and Taiwan, also posted new highs. The move appears to reflect investors pricing in the potential for continued disruption risks—such as supply disruptions through the Hormuz Strait—and concerns around renewed U.S.–Iran conflict.

Market participants also cited rapid progress in artificial intelligence as a key support for share prices of AI-related companies. This has helped underpin earnings growth that the market has already priced in, while contributing to higher GDP through increased private investment. Investors are also monitoring the possibility of a price rally if the United States and Iran reach a peace agreement, even though equities have already risen significantly since the cease-fire.

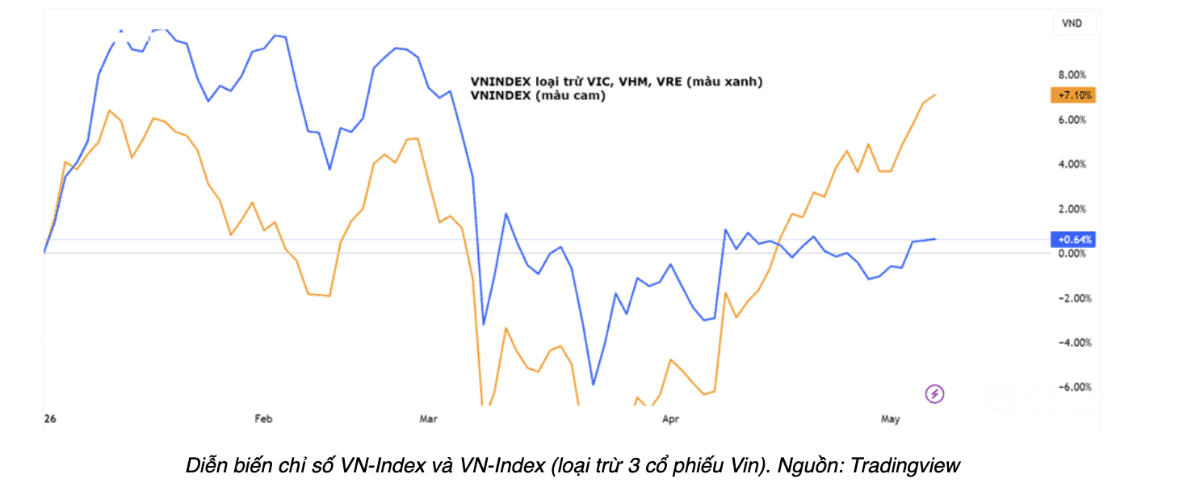

In Vietnam, trading resumed after the long holiday as the economy continued to grow, with GDP Q1/2026 estimated at approximately 7.83%. The VN-Index also posted new highs, driven primarily by the weight of large-cap stocks, notably VIC, VHM, and large banks.

However, breadth remained weak and liquidity was at a low base. Many stocks were red or traded sideways, and a large portion of investors remained in losses despite the index’s gains.

The market’s behavior has been described as a “K” shape: a small group of large stocks dominates index performance, while the rest of the market—and the real economy—appear out of sync. Investors are therefore focusing on whether liquidity and sector participation can broaden beyond the current leadership group, which has been concentrated around the Vingroup cohort.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…