•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

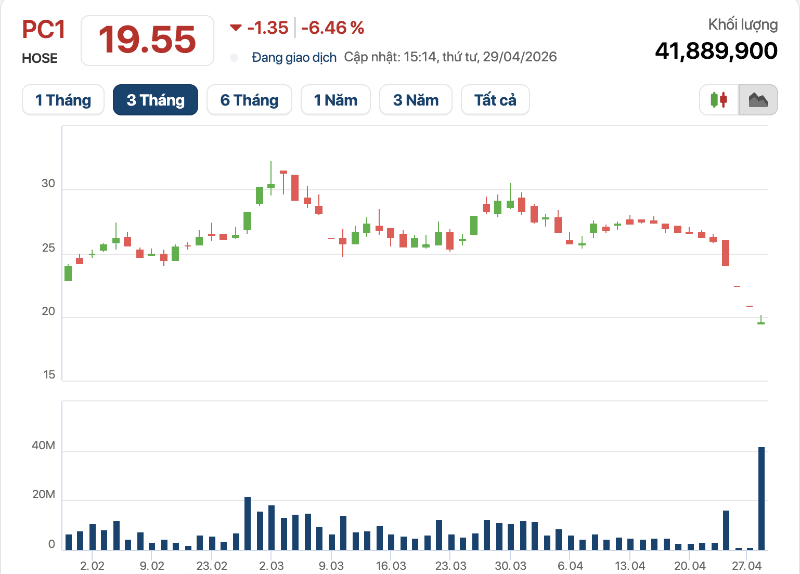

PC1 stock closed near the floor price on April 29, 2026, after opening higher earlier in the session and then sliding toward last October’s low. By the close, selling pressure remained strong enough to outweigh buying interest, with PC1 finishing at 19,550 dong per share, just above the floor price of 19,450 dong per share.

Trading volume reached nearly 42 million shares, the highest liquidity in PC1’s history. In the morning, total matched volume for the code was about 34.2 million shares, equivalent to roughly 8.3% of the listed volume.

In recent sessions, PC1 shares were repeatedly sold off. A gap between buyers and sellers appeared as at-floor supply accumulated to nearly 29 million shares, indicating investors are attempting to exit amid unverified negative information circulating about the company.

Selling pressure pushed the price lower for nine consecutive sessions, including three sessions (April 23, 24, and 28) that ended at the floor price.

By the end of 2025, PC1’s total assets exceeded 24,500 billion VND, up about 3,500 billion VND from the prior year. Cash and cash equivalents topped 5,200 billion VND, representing about 21% of total assets and up 64% since the start of the year. However, a significant portion of this cash is used as collateral for bank loans.

Operating cash flow in 2025 recorded a surplus of over 2,200 billion VND, more than doubling year-on-year, supported by construction and power generation activities. Total financial debt stood at over 11,700 billion VND, about 2.8 times equity, while total liabilities accounted for 64% of total capital. Short-term debt due within the next 12 months exceeded 1,100 billion VND, creating near-term repayment pressure.

PC1 also disclosed USD-denominated funding from foreign banks with maturities from 2030 to 2035, which can introduce foreign-exchange risk if the domestic currency depreciates against the USD.

Beyond bank loans, PC1 issued 1,200 billion VND in bonds to invest in industrial real estate development, including through purchases of existing shares and new issues of Western Pacific Joint Stock.

High leverage contributed to financing costs in 2025 exceeding 815 billion VND, including interest expenses and FX losses.

Statistics cited show debt outstanding rose sharply from 3,700 billion VND at the end of 2020 to over 11,700 billion VND after five years, an increase of more than 200%. The growth was attributed to long-term credit facilities from foreign banks and financial institutions.

To reduce the debt burden and bolster working capital, PC1 carried out a capital increase from existing shareholders, which helped “beautify” the balance sheet and ease debt pressure.

According to PC1’s 2025 annual report, the company had more than 411 million shares outstanding and over 29,000 shareholders, including 144 institutional investors and more than 28,900 individual investors.

Domestic shareholders held about 344.6 million shares (around 83.8% of PC1’s capital), while foreign shareholders owned 16.21%.

Chairman Trịnh Văn Tuấn was the single largest shareholder with nearly 88 million shares at end-2025, equivalent to about 21.38% of the company’s capital.

Securities VI VIX previously held 5.79% but sold 3 million shares in September 2025 to reduce its stake to 4.95%, meaning VIX no longer remains a major shareholder.

The BEHS group was also previously reported as a large shareholder; by January 2024 it had disposed of all more than 73 million PC1 shares, reducing ownership from 23.6% to 0%. The transfer value at that time was about 1,870 billion VND, with an average price of 25,460 VND per share.

PC1 is among Vietnam’s leading EPC contractors in the construction of transmission lines and substations, with more than 60 years of experience. In industrial production, PC1 is the sole unit and the largest in Vietnam for the design and manufacture of 110 kV and 220 kV single- and multi-core steel towers, as well as braced steel towers up to 750 kV.

Bitcoin (BTC) investors who use steady dollar-cost averaging (DCA) may be underperforming versus strategies that adjust exposure to the market’s cycle, according to new research arguing that Bitcoin’s behavior differs from traditional long-duration assets.

In a report cited by Markus Thielen of 10x Research, Bitcoin’s market…