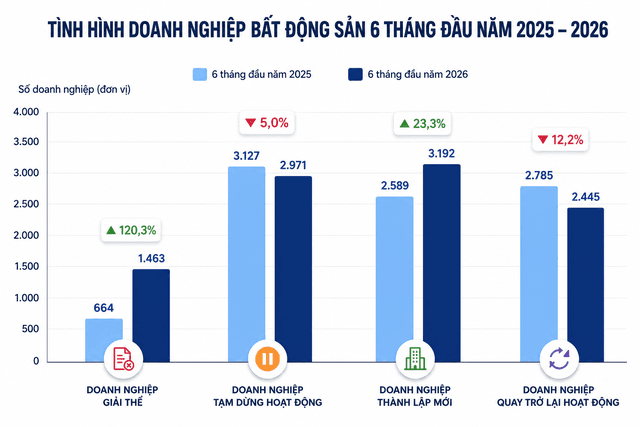

The data, released by the General Statistics Office (Ministry of Finance), shows that in the first six months of the year, the country had 1,463 real estate companies completing dissolution procedures, up 120.3% year-on-year. This is the highest increase among indicators reflecting the real estate business activity.

Additionally, 2,971 companies suspended operations, equivalent to 95% of the same period last year. Conversely, 3,192 new companies were established, up 23.3%, while 2,445 companies returned to operation, 87.8% of the same period.

These figures show the ongoing screening in the sector. While the number of entrants to the market continues to rise, the pace of exits, especially dissolutions, is rising faster, reflecting competition pressure and ongoing restructuring.

Notably, this occurs in the context of foreign capital continuing to attract attention to the real estate sector. According to the Ministry of Finance, total foreign direct investment (FDI) registered in Vietnam in the first six months reached $34.65 billion, up 61% vs the same period last year. Of this, real estate attracted about $5.1 billion, becoming the second-largest recipient after manufacturing.

This continues the trend from the previous year, when the real estate sector attracted $6.26 billion in FDI, accounting for 19.9% of total newly registered and adjusted capital.

The continued rise in foreign capital while domestic companies dissolve at a rapid pace reflects diverging views among investor groups. While many domestic firms face cash-flow pressure, cost of capital, and purchasing power constraints, foreign investors continue to expand their presence with long-term growth potential for Vietnam’s market.

However, the surge in foreign capital does not mean the real estate market is entering a hot growth cycle. Rather, this development arrives as domestic buyers shift from readiness to pay to a wait-and-see stance.

Batdongsan.com.vn market data show that nationwide interest in real estate in May fell about 5% month-on-month.

A recent survey also indicates only about 36% of respondents still maintain clear demand for real estate, down significantly from 55% last year. Notably, only about 17% plan to buy real estate in the next six months, while most choose to wait at least another year before deciding.

Not only demand is waning, but price levels in some areas have begun to show signs of adjustment. In May, the average apartment price in Hanoi fell from about 88 million VND per square meter to 85 million VND/m² after a few months. In Ho Chi Minh City, the average price remained around 69 million VND/m², nearly flat versus the prior quarter. Meanwhile, listing prices for apartments in Hung Yen and Bac Ninh also declined by about 3%.

Experts say this development shows foreign investors still place faith in the long-term prospects of Vietnam’s real estate market, while domestic individual buyers prefer to observe interest-rate trends, supply, and price movements before committing.

A new industry report by MBS Research also suggests the market is likely to continue facing notable challenges in the remaining months of the year as lending rates stay high while new supply continues to enter the market.

According to MBS Research, in Q2, deposit rates at many banks rose by about 1-1.5 percentage points compared with the previous quarter, pushing typical real estate loan rates to around 13-14% per year, up about 2 percentage points year-on-year.

To support purchasing power, many developers in Hanoi, Quang Ninh, and Ho Chi Minh City have rolled out programs to support interest costs, fixing loan rates at about 7-8% per year for the first two years for borrowers. However, MBS Research notes these programs mainly help ease financial pressure in the early stage, while buyer sentiment remains influenced by expectations that interest rates will stay high for some time.

On the market side, OneHousing notes the average absorption rate of primary projects in the first half is around 50-60%, a significant drop from over 80% in the same period last year.

This indicates the market is entering a deeper screening phase after a period of hot growth. While previously the advantage belonged to developers with scarce supply, now competition hinges on real project value, product quality, and transparency of legal status.

Research indicates that the recovery outlook will depend not only on interest-rate movements but also on supply quality, legal progress, and the ability to rebuild buyers’ confidence.

That also implies the recovery process will likely unfold with clear differentiation. Companies with solid financial foundations, transparent legal status, and products that meet real demand are expected to have more advantages in the next development cycle of the market.