•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

At the close of trading on April 29, 2026, the VN-Index ended at 1,854.10 points, up 1.37% from three months earlier. Meanwhile, the HNX-Index and UpCOM-Index fell 2.14% and 1.70%, respectively. While the overall index moved modestly, the market showed notable sectoral divergence.

The real estate group led gains by about 39%, mainly driven by VinGroup-related stocks. In contrast, broad-based downside pressure appeared across other sectors, notably utilities (-28%), software technology (-27%), and banks (-10%).

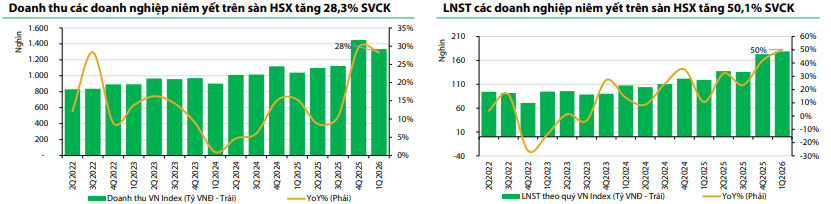

In a recent strategy report, VDSC highlighted the brightest market signal coming from the Q1 2026 earnings season. For the VN-Index basket, total market revenue rose about 28.3% year-on-year, while net profit rose 50.1% and net profit margin improved to 14.7%. Profit growth was mainly concentrated in real estate, energy, banking, and materials.

According to VDSC, the market remains cautious even as Q1 2026 earnings grew strongly. The index’s upward momentum was mainly driven by a few individual stocks, while overall valuation multiples did not expand commensurately with the earnings base. This suggests investors remain wary about the durability of the upturn, especially with high interest rates and energy price risks not fully cooling.

VDSC expects market dynamics to be influenced significantly by the Middle East situation. Oil supply disruption risks persist but are unlikely to endure long, as the cost of sustaining conflict rises for all parties involved. The backwardation in oil prices—where near-term futures prices are lower than longer-term futures—partly reflects expectations that geopolitical tensions may ease in the medium term.

Domestically, Q1 2026 GDP rose 7.83% year-on-year, the highest since 2011, but still below the government target of 9.1%. VDSC believes continued high growth in the remaining quarters will keep policy focused on public investment and capital inflows to support the economy. However, a weak trade balance and high interest rates remain risks for exchange-rate stability and bank loan quality.

Regarding profit outlook, the market-wide net income in Q2 2026 could rise by about 18% year-on-year, led by real estate and banking. Real estate is expected to benefit from a low base and improved project execution, while credit growth will continue to support banks despite net interest margin pressure.

Based on this, VDSC trimmed the VN-Index’s target P/E range to 12.2x–14.0x for the 3–4 months ahead, reflecting the view that interest rates are unlikely to return to low levels soon. The VN-Index is anticipated to fluctuate in a range of about 1,623–2,317 points, implying a swing of -10.7% to +24.9% from the close on 29/04/2026. While a strong valuations expansion phase is not expected soon, VDSC believes medium-term recovery room remains if geopolitical tensions ease and domestic policy support proves effective.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…