A 0% interest rate on USD deposits may seem like the end of foreign-currency mobilization, but in reality it reveals a paradox. Since 2016, Vietnam’s banking sector has pushed USD deposit rates to 0% to encourage holding VND. At the same time, the State Bank of Vietnam (SBV) has used policy tools to curb foreign-currency hoarding, including restrictions on USD purchases when there is no real demand and daily management of the central exchange rate. The approach is intended to reduce speculation expectations and restrain dollarization.

In the common process described, enterprises and individuals with foreign currency sell to credit institutions, which then sell back to the SBV. This helps strengthen foreign exchange reserves. Authorities have repeatedly warned that raising interest on foreign-currency deposits would give holders both exchange-rate gains and deposit interest, potentially encouraging capital to shift from VND to foreign currency and increasing risks to the foreign exchange market.

In practice, demand to hold USD is not determined solely by interest rates. In a context of global economic volatility, many individuals and businesses still hold foreign currency as a hedge. The key factor is the expected exchange rate, which acts as a form of “hidden yield” that can replace the nominal 0% cash rate. When USD strengthens against VND, holders can realize financial gains without receiving bank interest.

This creates a challenge for banks that rely only on residents selling USD when the exchange rate rises, while other parts of the market still demand foreign currency. Banks therefore pivot to more flexible solutions, including allowing customers to use USD as collateral to borrow VND at low cost.

One common approach is to let customers keep USD in banks as collateral rather than convert it into VND. In some cases, loan rates are around 1.8% per year, with limits up to the full value of USD deposits and short tenors, usually not more than six months. The structure is described as a two-way capital rotation between USD and VND, enabling both customers and banks to leverage their respective advantages.

Risk is described as being tightly controlled because the collateral is USD, which is characterized as a relatively safe, standardized asset. If a client defaults, the bank can liquidate the collateral by converting USD to VND at the prevailing rate to recover the loan.

A veteran personal-credit professional with years of experience at a Big 4 bank cautions that the risk is not small. For floating-rate loans, if VND interest rates rise, customers’ debt-service costs increase. Conversely, if USD depreciates, the value of the USD collateral declines, which can affect the safety of the loan for the bank.

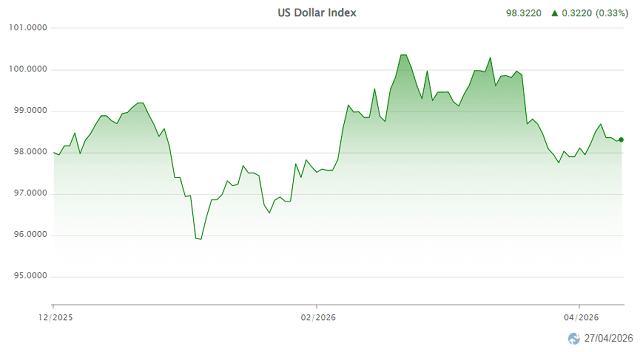

The article links renewed USD appeal to intensifying geopolitical tensions in the Middle East. The Dollar Index (DXY) has risen nearly 3% since the outbreak of the conflict, reaching about 100.36 points—the highest in almost 10 months—on March 13. After peaking, the DXY pulled back but remained around 100, the highest level since late November 2025.

VCBS commentary suggests that with geopolitical tensions showing no clear easing, the DXY is likely to remain on an upward trend. It cites both defensive psychology and fundamentals supporting the dollar, noting that the United States is a net energy-exporting country. If oil and gas prices continue rising due to supply disruptions, the US energy balance could improve relative to net importing economies, reinforcing the greenback.

VCBS also assesses that a reversal toward a stronger USD would pressure the USD/VND exchange rate. It points to potential intensification in demand for importing raw materials and hedging/stockpiling psychology for USD. The pressure could grow if markets expect the Fed to keep rates higher for longer than anticipated.

Because Vietnam is a net energy importer, the article notes Vietnam could face a “double hit” from currency movements and international commodity prices, potentially fueling inflation in upcoming quarters if geopolitical tensions persist.

In response to rising exchange-rate pressure, on March 24 NHNN announced measures to intervene in the foreign exchange market by providing 180-day USD forward contracts with an option to cancel. The forward rate was set at 26,850 VND/USD, higher than the spot rate of 26,360 VND/USD. The article states this tool has been used for the third time since August 2025 to stabilize the rate.

According to Maybank Investment Bank, the forward sale tool is activated when VND faces renewed pressure—after declining about 1.2% from the beginning of the month—while USD rose about 2.1% over the same period.

The article also notes recent moves showing state-owned banks raising VND deposit rates, reflecting willingness to accept higher rates to defend the domestic currency. It contrasts this with late-2025 seasonal tightening, describing the current rate hikes as mainly driven by external pressure, similar to 2022 when USD strengthened and inflation risks prompted a government response.

In this scenario, the article says USD/VND and VND interest rates are moving higher together. When VND rates rise to defend the currency, borrowers using USD as collateral to borrow VND must calculate the break-even point carefully. If the exchange rate does not move as strongly as the interest rate increases, holding USD with VND-denominated debt could lead to a double loss—opportunity cost and interest costs.