•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Real estate remains the dominant collateral asset across Vietnam’s banking system, from private commercial banks such as VPBank, Sacombank and MSB to state-owned lenders including Vietcombank, Agribank, BIDV and VietinBank. The latest figures for 2025 and Q1-2026 show collateral values rising, with real estate continuing to play a leading role—highlighting both the potential “safety cushion” in lending and the need for careful risk management.

In many banks, real estate is the main collateral type, reflecting the continued importance of land assets in Vietnam’s credit market. At the same time, the data point to differences in each bank’s credit strategy, risk concentration, and how capital buffers are built around secured lending.

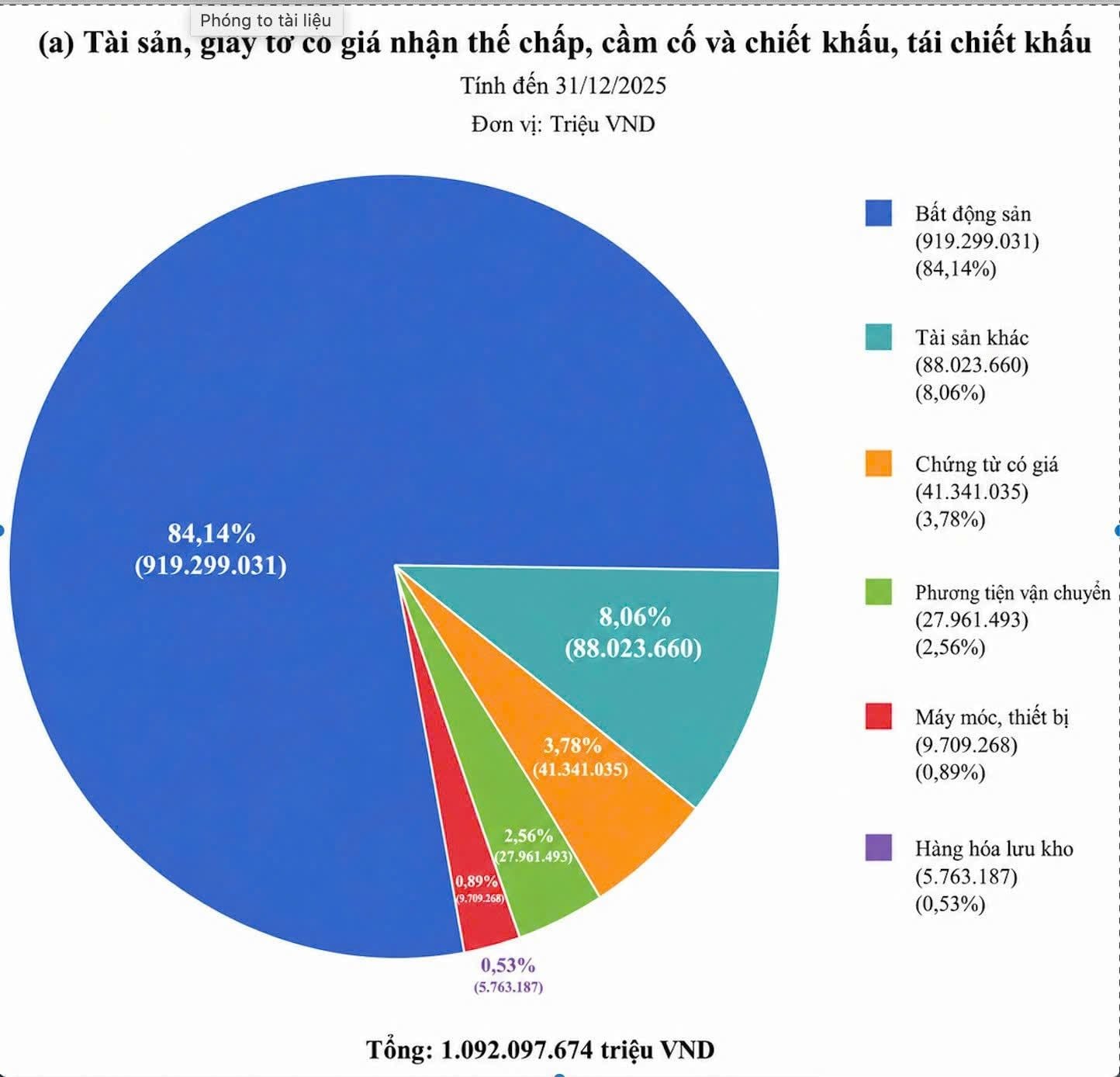

Sacombank’s financial report shows that at end-2025, total collateral value for loans reached over 1.09 quadrillion VND, up 14.5% from the start of the year and equal to about 174% of lending. Real estate accounts for about 919.3 trillion VND, representing 84.2% of total collateral value and up 10% versus the same period.

MSB’s collateral portfolio at end-2025 stood at 559.311 trillion VND, equivalent to 272% of lending. In MSB’s collateral mix, real estate accounts for about 42% (over 235.0 trillion VND). Unlike banks that concentrate heavily in real estate, MSB’s collateral structure is more diversified, with the remainder comprising debt instruments, vehicles and other assets.

For VPBank, the value of collateral as of 31-3-2026 reached about 3,049 trillion VND, up 10.7% from end-2025. Within the collateral structure, real estate exceeds 719.0 trillion VND (about 23.6% of total collateral), while other collateral assets total nearly 2.15 quadrillion VND, accounting for about 70.5% of total collateral. Relative to the industry pattern where real estate typically dominates, VPBank’s real estate share is comparatively lower.

The four state-owned banks—Vietcombank, VietinBank, BIDV and Agribank—also show real estate as a central collateral asset. Across these banks, total real estate collateral exceeds 10.6 quadrillion VND, accounting for about 76% of total collateral.

The figures reflect a market where land assets remain the most common form of collateral. The article raises the question of whether holding a large volume of real estate as collateral signals risk. From a risk-management perspective, many banks treat real estate collateral as a safety cushion—especially when collateral values exceed loan books.

Vietcombank’s management explains that total collateral for secured loans exceeds its loan book, indicating high asset quality and a strong safety cushion. The bank also maintains tighter controls on property-related products and prioritizes financing for industrial parks, export-oriented projects and social housing to balance risk and growth.

However, the downside risk remains: if the real estate market declines, collateral values could fall, potentially affecting debt recovery. Concentrating heavily in one asset class can also reduce portfolio flexibility.

Current data indicate that real estate will continue to be central in the collateral framework of the banking system. At the same time, diversification is increasing as banks seek to spread risk and selectively hold “quality” collateral with higher liquidity and stronger legal backing.

Premium gym chains are entering a “golden era” that is ending or already in decline, as rising operating costs collide with shifting consumer preferences toward more flexible, community-based ways to exercise. Long-term memberships are shrinking, margins are pressured by higher rents and facility expenses, and competition from smaller, more personalized…