•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

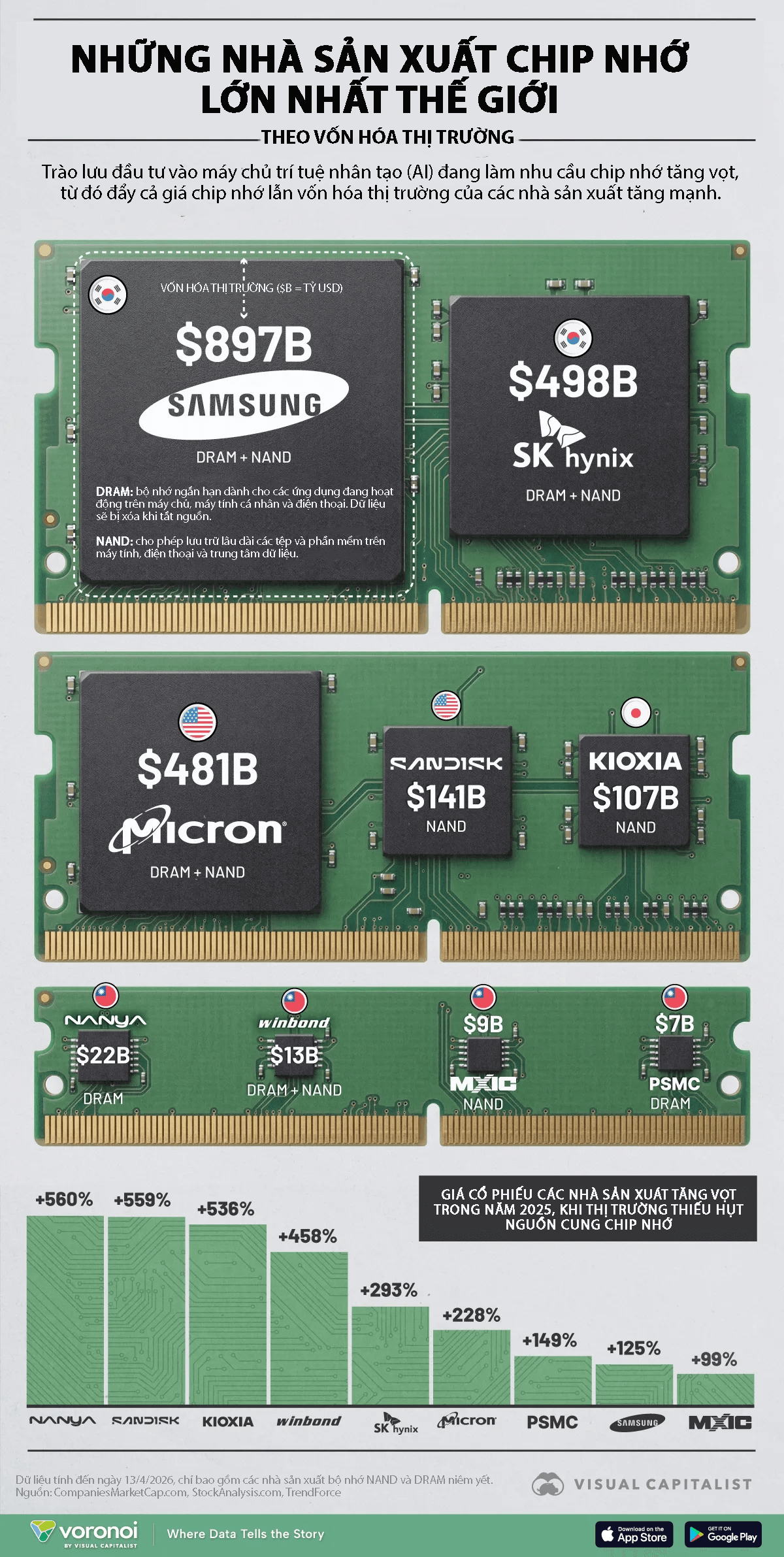

In recent years, global AI infrastructure investment has reshaped the semiconductor industry, boosting the market capitalization of memory-chip makers. Based on data available up to April 13, 2026 from CompaniesMarketCap and StockAnalysis, the infographic below lists the world’s largest memory-chip makers.

Samsung Electronics of South Korea leads by a wide margin, with a market capitalization of $897 billion. It is followed by SK Hynix at $498 billion and Micron at $481 billion. Together, the three firms form a clearly leading group in the memory-chip industry, far ahead of the rest of the rankings.

In the next tier, SanDisk (United States) and Kioxia (Japan) have market capitalizations of $141 billion and $107 billion, respectively. The remaining Taiwanese companies listed are Nanya ($22 billion), Winbond ($13 billion), Macronix ($9 billion), and Powerchip Semiconductor Manufacturing ($7 billion).

Analysts say that in 2025 memory-chip prices rose sharply because producers did not increase output while demand tied to AI infrastructure grew rapidly, tightening supply. This environment helped memory-chip makers raise prices more readily and increased investors’ expectations.

Stock prices of memory-chip producers rose sharply in 2025. Notably, Nanya shares rose 560%, SanDisk rose 559%, and Kioxia rose 536%. Winbond, SK Hynix, and Micron also posted notable gains.

The trend continued into 2026. From the start of the year through April 17, Samsung rose 80%, SK Hynix rose 73%, and Micron rose 59%.

Memory chips mainly consist of two types: DRAM and NAND. DRAM is temporary memory used to store data for immediate processing and is lost when power is off. NAND is long-term storage that can store files and software even when the device is not powered.

While both DRAM and NAND are essential to modern computing, the growth of AI data centers is making high-performance memory more strategically important. As a result, the outlook for memory-chip makers is no longer tied only to the consumer electronics cycle, but increasingly depends on the expansion of AI data centers.

Coinbase has launched a High Yield USDC vault within its in-app DeFi lending offering, adding a second lending option that provides exposure to a wider range of collateral assets. The product is powered by Morpho infrastructure and uses vault allocations curated by Steakhouse Financial.